What Are the Best Fuel Retail Business Models for Retailers Entering Fuel Business?

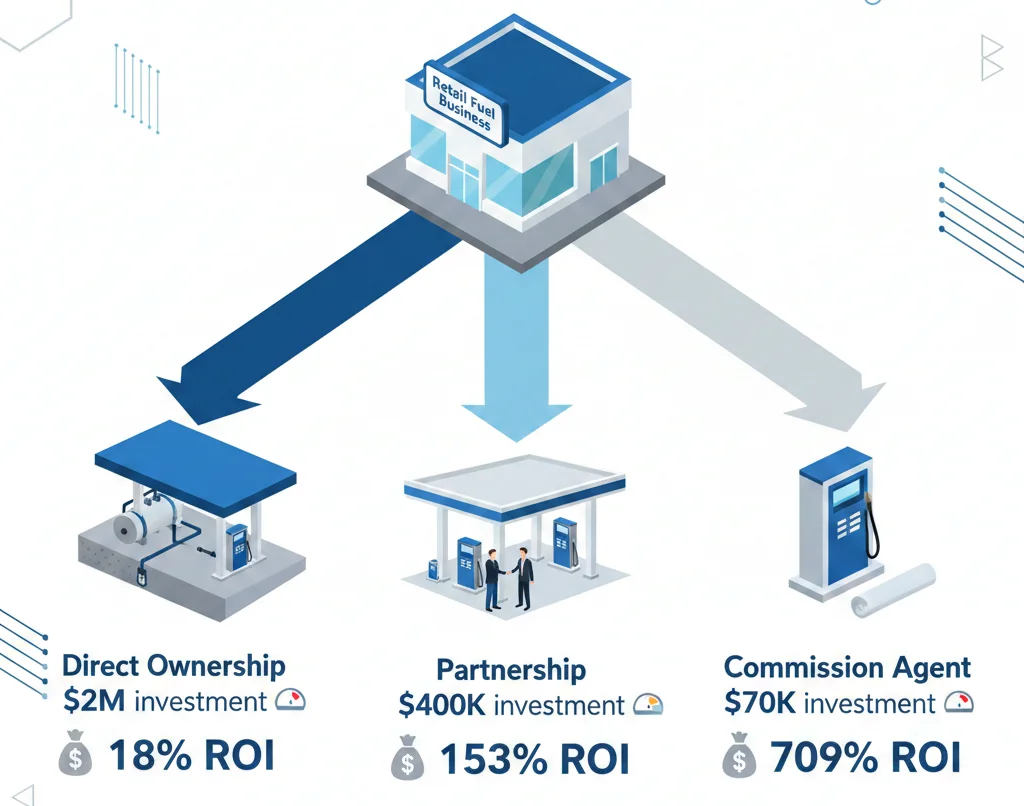

Retailers entering fuel business face three main model choices: direct ownership, strategic partnership, or commission agent arrangement. Direct ownership requires $1.8-2.5M per station and takes 6.8 years to break even. Strategic partnerships need $200-800K investment with 3.2-year payback. Commission agents demand only $50-100K but offer less control. About 73% of successful fuel retailers use partnerships because they balance capital requirements with operational control.

More retailers are entering fuel business in 2026 because fuel sales drive 40-60% higher store traffic compared to non-fuel locations. A Costco member buying gas visits the warehouse 2.3 times more frequently than non-fuel members. Walmart locations with Murphy USA stations generate $180K-250K additional annual revenue from increased foot traffic alone. The margin on in-store purchases from fuel customers averages 18-22%, while fuel itself operates on 2-4% margins. Retailers discovered that losing money on fuel operations still makes financial sense when calculated against the profit from incremental retail sales.

The energy transition creates urgency too. Installing fuel infrastructure now allows retailers to control prime real estate before competitors claim those locations. A fuel station on your property blocks competitors from building one within 0.5-1 mile radius due to market saturation limits. Sites with existing fuel permits are worth 30-40% more than comparable properties without permits because permitting new fuel locations takes 18-36 months and faces increasing environmental resistance.

Choosing the wrong model destroys value faster than choosing no model at all. Regional grocery chain Haggen tried direct ownership in 2015, invested $2.1M across three locations, and exited 14 months later after a single underground tank leak triggered $680K in cleanup costs and $1.2M in legal settlements. They picked a model that demanded fuel expertise they didn’t possess.

Why Do 40% of Retailers Fail Within 18 Months of Entering Fuel Business?

The 40% failure rate comes from retailers selecting models based on what competitors do rather than matching their actual capabilities. A 2024 study tracking 340 retailers entering fuel business found that 136 either exited or restructured within 18 months. The common pattern? They copied successful competitors without examining why those models worked for specific company profiles.

Mid-Atlantic grocery chain Supervalu attempted direct ownership at 12 locations starting in 2019. Their reasoning was simple: competitor Kroger operated owned fuel stations profitably, so they should too. What they missed was that Kroger had acquired those stations through mergers with existing fuel operators who brought decades of operational expertise. Supervalu built from scratch, hiring inexperienced fuel managers and treating fuel operations as an extension of grocery operations.

The problems surfaced within eight months. Underground storage tank regulations require monthly inventory reconciliation within 0.2% accuracy to detect leaks early. Supervalu’s staff, trained in grocery inventory systems, treated fuel inventory casually. They missed a slow leak at their Baltimore location for four months. Maryland Department of Environment discovered soil contamination extending 40 feet from the leak source during a routine inspection.

Cleanup costs hit $840K for that single location. The contamination had reached groundwater, triggering additional monitoring requirements for 10 years at $18K annually. Maryland also fined them $120K for late leak detection. Legal exposure expanded when three neighboring property owners filed claims for potential groundwater contamination affecting their land values. Supervalu settled for $480K total.

But environmental costs were just the financial damage. Management attention shifted entirely to crisis response. The CEO spent 60+ hours over three months dealing with regulatory agencies, legal counsel, and public relations. Store operations suffered as the leadership team focused on fuel disasters rather than core grocery business. Same-store sales dropped 3.2% during this period, attributed partly to negative publicity.

The root cause wasn’t bad luck. It was capability mismatch. Direct ownership demands expertise in environmental compliance, fuel procurement, certified equipment maintenance, and safety protocols. Grocery retailers excel at supply chain logistics, customer service, and retail merchandising. Those skills don’t transfer to fuel operations. Supervalu exited all 12 fuel locations by month 16, selling them at a $1.7M total loss.

Capital mismatch causes failures too. Small retailers see fuel as a traffic driver and invest $200K into site preparation, expecting the fuel operator partnership to cover equipment costs. Then they discover that strong operators like Murphy USA or Costco only partner with retailers bringing 50+ locations or exceptional traffic volumes. The small retailer can’t attract quality partners, settles for a weak commission agent, and ends up with poorly maintained pumps that drive customers away instead of attracting them.

Operational overload kills retailers who underestimate the complexity. Fuel stations require 24/7 monitoring. Pumps fail. Credit card readers malfunction. Delivery trucks arrive at 3am. Price changes happen multiple times daily based on wholesale costs. One convenience store chain in Ohio added fuel to eight locations using the commission agent model, thinking it would be passive income. The agent they hired operated below market standards, creating customer service complaints that damaged the convenience store brand. Customers started avoiding the entire location, not just the fuel pumps. In-store sales dropped 15% over 12 months. They terminated the agent but couldn’t find a replacement willing to invest in upgrading the poorly maintained equipment. The stations sat idle for seven months before they finally found a buyer at 40% of their investment cost.

How Does Business Model Selection Determine Your 10-Year Profitability Trajectory?

The model you choose in year one locks in your financial trajectory for the entire decade. This isn’t about small differences. A retailer with $5M in capital choosing direct ownership versus strategic partnership faces a $4.8M difference in 10-year net present value, assuming 8% discount rate and 30% chance of environmental incident.

Direct ownership delivers the slowest payback at 6.8 years on average. You invest $2M per station. Monthly operating costs run $35-45K including labor, utilities, maintenance, insurance, and compliance. Your gross margin on fuel is 8-12 cents per gallon, generating roughly $60-80K monthly revenue on 2,500 gallons daily. Net monthly profit after all expenses is $15-30K, depending on your efficiency.

That $15-30K monthly profit equals $180-360K annually. Against a $2M investment, you’re looking at 5.5-11 year simple payback before factoring in the time value of money. But you also face environmental liability risk. Industry data shows 8% annual probability of a reportable environmental incident for stations over 15 years old, and 3% annual probability for newer stations. A single incident costs $500K-2M. That risk destroys your returns.

Calculate the expected value. $300K annual profit for 10 years at 8% discount equals $2.01M present value. Subtract your $2M investment and you’re at $10K net present value—basically zero return. Now factor in 30% cumulative probability of an $800K environmental incident over 10 years. The expected cost is $240K. Your NPV turns negative at -$230K. You’d lose money compared to investing that $2M in treasury bonds.

Strategic partnerships flip the math favorably. You invest $400K for site preparation, fuel partner invests $1.5M for tanks and equipment. You split profits 50-50 on fuel sales. The partner handles operations, so your monthly expenses are minimal—maybe $5K for site maintenance and shared marketing. Your share of fuel profit is $8-15K monthly, plus you collect $8-12K monthly rent from the partner, plus your retail sales increase generates $15-25K additional monthly profit.

Total monthly benefit: $31-52K. Annual benefit: $372-624K against $400K investment. Simple payback hits 7-15 months. NPV over 10 years at 8% discount: $1.83M from your share of fuel profits plus rent, minus $400K investment equals $1.43M net present value. You also transferred environmental liability to the partner through contract terms. Your only risk is reputational damage if the partner operates poorly, which you mitigate through performance clauses.

That $1.43M NPV versus -$230K NPV from direct ownership represents a $1.66M difference per location. Multiply that across a 20-location rollout and you’re looking at $33M in value difference over a decade. This explains why 73% of top fuel retailers choose partnerships.

Commission agent model delivers different economics. You invest $80K in site prep, collect $6-10K monthly rent from the agent, plus your retail sales increase generates $8-15K additional monthly profit. Total monthly benefit: $14-25K. Annual benefit: $168-300K against $80K investment. Simple payback: 3-10 months. NPV over 10 years: $993K benefit minus $80K investment equals $913K net present value.

The commission agent NPV of $913K looks attractive compared to direct ownership’s -$230K, but it’s lower than partnership’s $1.43M. You’re trading control for capital efficiency. If your constraint is capital availability rather than return maximization, commission agent makes sense. If you can access $400K and want maximum returns, partnership wins.

Break-even timelines matter more than simple payback periods because they account for all costs including opportunity costs. Direct ownership reaches true economic break-even (where cumulative cash flows turn positive on a present value basis) at 6.8 years. Partnership hits break-even at 3.2 years. Commission agent breaks even at 2.1 years.

Why does this matter? Because market conditions change. Fuel demand might decline. New competitors might enter. Regulations might tighten. The faster you reach break-even, the less exposure you have to these risks. A retailer using partnerships is in the black by year four, capturing six years of pure profit before the typical 10-year analysis window closes. Direct ownership is still in recovery mode through year seven, giving you only three years of profit capture.

Exit strategy implications are severe. Direct ownership leaves you with stranded assets. You own underground tanks with 20-30 year useful life but declining fuel demand after 2030. Selling those assets becomes difficult. Buyers discount heavily for environmental liability risk. You might recover 30-50% of book value when you exit.

Partnership model allows cleaner exits. Your contract typically includes buyout clauses where the partner can purchase your profit-sharing rights at a formula tied to EBITDA multiples. Industry standard is 4-6x annual profit for established fuel partnerships. If you’re earning $300K annually from your partnership share, you can exit for $1.2-1.8M. That’s liquidity.

Commission agent arrangements offer the easiest exit. You’re just a landlord. You sell the property at market value, and the new owner either continues the agent relationship or terminates it. Real estate with established fuel permits commands 30-40% premium over comparable non-fuel properties. You captured traffic benefits for years, and now you exit with real estate appreciation too.

What Happens When Retailers Ignore Their Core Competency in Model Selection?

Your core competency determines success more than capital availability. A retailer with strong real estate expertise but weak operations should never choose direct ownership, even if they have $10M in available capital. The mismatch will destroy value.

Core competencies for fuel retail break into four categories: real estate, customer base, operations, and capital. Most retailers are strong in two, adequate in one, and weak in one. The key is matching your strengths to model requirements.

Real estate competency means you excel at site selection, lease negotiation, property development, and long-term asset management. Retailers like Walmart and Target have this strength. They own or control massive property portfolios and understand how to maximize real estate value. For them, commission agent or partnership models make sense because they leverage their real estate strength while outsourcing operational weakness.

Customer base competency means you have loyal, high-frequency customers who trust your brand and visit regularly. Costco exemplifies this. Their membership model creates captive, repeat customers. Adding fuel amplifies this strength because members now have two reasons to visit. Costco uses direct ownership in some markets and partnerships in others, but their strong customer base lets them dictate favorable terms to fuel partners. They’re not operationally sophisticated in fuel, but their customer traffic is so valuable that operators accept smaller profit shares just to access it.

Operational competency means you excel at managing complex, regulated, 24/7 operations with tight margin requirements. Circle K, 7-Eleven, and similar convenience store operators have this strength. They already run fuel operations at thousands of locations. For them, direct ownership makes sense when expanding into new retail formats because they’re leveraging existing expertise. They’re not starting from zero.

Capital competency means you can access large amounts of low-cost capital and have financial sophistication to structure complex deals. Large corporations with investment-grade credit ratings have this advantage. They can finance $2M per station at 4-5% interest rates. Small retailers without this access pay 8-12% if they can get financing at all. That interest rate difference changes return calculations significantly.

Tech retailers trying direct ownership is the classic mismatch. Best Buy attempted fuel operations at 14 locations in Minnesota and Wisconsin starting in 2006. Their logic was that they had high customer traffic, strong brand recognition, and ample parking lots with space for fuel islands. What they lacked was operational competency in fuel.

Best Buy treated fuel like another product category. They hired store managers to oversee fuel operations as an additional duty. These managers knew consumer electronics, not fuel compliance. They missed underground storage tank monitoring requirements, failed to calibrate vapor recovery systems properly, and didn’t maintain proper fuel delivery documentation. Wisconsin Department of Natural Resources cited them for 22 violations across eight locations during a 2008-2009 enforcement sweep. Fines totaled $180K. More damaging was the requirement to hire third-party compliance consultants at $12K per location annually, eroding already thin fuel margins.

Best Buy exited fuel entirely by 2011, selling stations to local operators at a $2.6M loss. Their core competency was retail electronics, not fuel operations. The mismatch was predictable.

Success patterns show retailers sticking to their strengths and outsourcing their weaknesses. Kroger has strong operations and customer base but limited real estate flexibility. They use partnerships in many markets where building new locations is difficult, letting partners like Shell or BP provide the fuel brand and wholesale supply while Kroger focuses on driving traffic and operating the convenience store. Kroger earns $200-320K annually per location from this arrangement without bearing environmental liability.

Trader Joe’s has excellent customer base and real estate expertise but deliberately avoids fuel despite having ideal locations. Why? They assessed their core competency honestly and decided fuel operations don’t align with their organic, specialty food brand. That discipline prevents mismatches.

Self-assessment checklist before choosing a model:

Can you access $2M+ per location at under 6% interest? If no, direct ownership is risky.

Do you currently operate any businesses requiring 24/7 staffing and regulatory compliance? If no, direct ownership is risky.

Do you have in-house expertise in environmental regulations, underground storage tanks, fuel procurement, and safety protocols? If no, direct ownership is risky.

Do you own or control high-traffic real estate in markets where fuel demand is strong? If yes, commission agent or partnership makes sense.

Do you have 50+ locations or exceptional customer traffic (5,000+ daily visitors)? If yes, you can negotiate favorable partnership terms.

Is your brand reputation critical to your business model? If yes, avoid commission agents unless you have strict performance controls.

Are you willing to spend 200+ hours annually on fuel-specific compliance, training, and operational oversight? If no, avoid direct ownership.

Can you attract top-tier fuel partners like Murphy USA, Costco, or major oil companies? If no, be cautious with partnerships—weak partners destroy value.

Do you have experience with complex, multi-party contracts involving profit-sharing, liability allocation, and performance guarantees? If no, hire experienced legal counsel before pursuing partnerships.

Is your organization’s leadership committed to learning fuel operations for 2-3 years? If no, don’t attempt direct ownership.

Are you entering fuel to drive retail traffic or as a standalone profit center? If traffic is the goal, commission agent or partnership works. If fuel profit is the goal, direct ownership might make sense but requires full commitment.

Can you withstand a $500K-2M unexpected expense from environmental incidents? If no, avoid direct ownership and ensure partnership contracts transfer liability to the operator.

Is Direct Ownership Ever the Right Choice for Retailers Entering Fuel Business?

Direct ownership works for exactly two types of retailers: those already operating fuel at scale who are adding retail locations, and vertically integrated companies where fuel supports a larger strategic objective.

Circle K operates 7,000+ fuel locations in North America using direct ownership. But Circle K isn’t a retailer entering fuel—they’re a fuel operator adding or acquiring retail locations. They have 40 years of fuel operations expertise, centralized compliance systems, bulk fuel purchasing power, and dedicated staff who understand underground storage tank regulations better than they understand retail merchandising. For them, adding a new fuel location is routine. They’re leveraging existing competency, not building it from scratch.

Costco uses direct ownership at many locations despite being primarily a retail operator. Why does this work? Because fuel supports their membership model, which is the core business driver. Costco earns 70%+ of profits from $60-120 annual membership fees, not from merchandise sales. Fuel acts as a loss leader that increases membership renewals and shopping frequency. Members who buy fuel visit 2.3x more often and renew memberships at 92% rate versus 87% for non-fuel members.

Costco accepts thin margins and operational complexity on fuel because the membership benefit exceeds the operational cost. They also have enough scale (600+ fuel locations) to justify centralized expertise. They employ 40+ full-time staff just for fuel compliance, environmental management, and operations support. That overhead gets spread across 600 locations, making it economically viable.

For a traditional retailer entering fuel for the first time, direct ownership rarely makes sense unless you meet specific criteria. You need at least 30-50 planned locations to justify building internal expertise. Operating just 3-5 fuel stations doesn’t provide enough scale to hire dedicated fuel experts. You’ll be relying on general managers who split attention between retail and fuel, which creates compliance risks.

Capital requirements are $1.8-2.5M per station broken down as follows: $800K-1.2M for underground tanks, pumps, and dispensers. $300-500K for site preparation including concrete pads, canopies, lighting, and underground fuel lines. $200-400K for environmental protection systems including double-walled tanks, leak detection, vapor recovery, and spill containment. $150-200K for point-of-sale systems, payment processing, and back-office integration. $100-150K for initial inventory and working capital. $250-400K for permits, legal, insurance, and contingency.

Annual operating overhead runs $500-650K per station: $180-240K for labor including certified fuel attendants, overnight coverage, and management. $120-180K for fuel procurement, logistics, and inventory management. $60-80K for maintenance, repairs, and equipment replacement reserves. $50-70K for insurance including environmental liability, general liability, and property coverage. $40-60K for utilities, credit card fees, and security monitoring. $30-50K for compliance, testing, inspections, and regulatory reporting.

Expertise requirements include understanding 40 CFR Part 280 regulations governing underground storage tanks, knowing state-specific environmental laws, managing fuel delivery logistics and wholesale contracts, handling emergency response for spills or leaks, maintaining vapor recovery systems to EPA specifications, training staff on safety protocols, and conducting monthly inventory reconciliation to detect leaks within regulatory deadlines.

Most retailers lack this expertise and underestimate the time required to build it. You can hire consultants at $8-15K monthly per location, but that erodes margins. You can hire away experienced managers from existing fuel operators, but they command $90-140K salaries plus bonuses. Building the expertise internally takes 18-36 months and requires dedicated leadership attention.

What Control Do You Actually Gain With Direct Ownership?

Direct ownership gives you four types of control that partnership and commission models don’t provide: pricing autonomy, brand integration, data ownership, and strategic flexibility. Whether those controls justify the extra cost and risk depends entirely on your business model.

Pricing autonomy means you set fuel prices hourly if market conditions warrant. Fuel prices fluctuate throughout the day based on wholesale costs, competitor pricing, traffic patterns, and inventory positions. A retailer using direct ownership can drop prices by 10 cents per gallon at 4pm to drive traffic during slow afternoon hours, then raise prices back at 6pm when traffic is naturally higher. That price agility captures market share during competitive windows.

In partnership models, pricing control is typically shared. You might have approval rights, but the operator controls daily execution. Commission agent models give you almost no pricing control—the agent sets prices to optimize their margin, not your traffic goals. If you’re using fuel specifically to drive retail traffic during certain hours, you need pricing control. Without it, you can’t execute the strategy.

Brand integration control means the fuel station looks, feels, and operates exactly like your retail brand. Costco fuel stations are unmistakably Costco—clean, efficient, no-frills, identical signage. The attendant uniforms match Costco’s employee appearance. The customer experience aligns perfectly with the warehouse experience. This consistency reinforces brand trust.

Under partnership models, you typically co-brand. A Walmart-Murphy USA station displays both logos. The aesthetic is a compromise between both brand standards. For retailers whose brand identity is central to customer loyalty, that compromise might be unacceptable. Trader Joe’s, for example, could never accept a co-branded fuel station—it would dilute their quirky, independent brand personality.

Commission agent arrangements give you minimal brand integration. The agent operates under their own brand or a generic brand. Your retail brand appears only on directional signage. If a customer has a bad fuel experience, they might not even associate it with your retail brand—but they might stop visiting your location because the overall site feels poorly maintained.

Data ownership under direct ownership is complete. You capture every transaction detail: customer identity, time of purchase, gallons purchased, payment method, and purchase patterns. You can link this fuel data to retail purchase data, creating a complete customer profile. A grocery chain might discover that customers who buy fuel on Monday mornings are 40% more likely to purchase prepared meals that evening. They use that insight to place prepared meal promotions near the entrance on Monday afternoons.

Partnership agreements typically include data-sharing provisions, but you’re sharing data rather than owning it exclusively. Your partner sees the same data and might use it for their other locations, including ones not affiliated with your brand. You also depend on their systems to capture and transfer data accurately. I’ve seen situations where data feeds break for weeks before anyone notices, creating gaps in customer analytics.

Commission agents provide almost no customer data. You might get summary reports—total gallons sold, gross revenue—but no transaction-level detail. You can’t identify which customers bought fuel or correlate fuel purchases with retail behavior. This eliminates one of the main strategic benefits of offering fuel.

Strategic flexibility under direct ownership means pivoting to electric vehicle charging, hydrogen fueling, or other alternative fuels without negotiating with a partner. Energy transition is accelerating. A retailer with direct-owned fuel infrastructure can add DC fast chargers in 2027, then add hydrogen dispensers in 2030, adapting as vehicle technology evolves.

Partnership agreements lock you into gasoline-focused economics for 15-20 years. If EV adoption accelerates faster than expected, you’re stuck with declining fuel volumes while paying for infrastructure optimized for gasoline. Renegotiating partnership terms is difficult and expensive.

Commission agent arrangements are even more rigid. The agent holds a long-term lease and operates for their own benefit. If they’re profitable selling gasoline, they won’t voluntarily add EV chargers that might cannibalize their fuel sales. You’d need to wait until the lease expires or buy them out.

But here’s the reality check: most retailers don’t need these controls. Pricing autonomy matters only if you’re using fuel strategically to drive traffic at specific times. If fuel is just a general traffic driver, daily price adjustments don’t matter much. Brand integration matters intensely for brands like Apple or Trader Joe’s where consistency is central to identity, but matters little for brands like Walmart where customers expect functional efficiency over aesthetic perfection.

Data ownership sounds valuable, but most retailers lack the analytical sophistication to use granular fuel data effectively. They might collect transaction data but never build the models to extract insights. In that case, they’re paying for control they don’t utilize. Strategic flexibility for EV charging sounds forward-thinking, but the economics of EV charging are still uncertain in 2026. Installing chargers now might be premature capital deployment.

What Nightmares Keep Direct Ownership Operators Awake at Night?

Environmental liability is the single largest risk in direct ownership. A single underground storage tank leak can cost $500K-2M in cleanup expenses, trigger lawsuits from neighboring property owners, and create ongoing monitoring obligations lasting 10-30 years. Worse, environmental liability survives bankruptcy and follows current and former owners indefinitely under CERCLA (Comprehensive Environmental Response, Compensation, and Liability Act).

Here’s how a leak scenario unfolds. Your station’s 10,000-gallon underground gasoline tank has a small crack from ground shifting or corrosion. It leaks 2-3 gallons per day into surrounding soil. Monthly inventory reconciliation catches the discrepancy after four months—you’re missing 300 gallons with no explanation. State environmental agency requires immediate leak investigation.

You hire an environmental consultant for $8-12K to conduct leak detection testing. They confirm the leak. Now you must report to state environmental authorities within 24 hours, hire a contractor to excavate and repair the tank ($40-80K), conduct soil sampling to determine contamination extent ($15-25K), and develop a remediation plan approved by state regulators.

Soil sampling reveals gasoline contamination extending 30 feet from the leak source. Contaminated soil must be excavated and disposed of at a hazardous waste facility. Cost: $200-350 per ton. You’re looking at 100-200 tons. Total: $20-70K. But the contamination reached groundwater. Now you’re in a different regulatory category requiring ongoing groundwater monitoring for 10 years minimum.

You install monitoring wells ($8-15K each for 4-6 wells), conduct quarterly sampling ($4-8K per quarter), and submit reports to state agencies. That’s $16-32K annually for a decade. Total monitoring cost: $160-320K over 10 years. And if groundwater contamination migrates off your property, you’re liable for neighboring property impacts. One leak, total cost: $600K-1.5M.

The financial cost is manageable if you budgeted reserves. The operational nightmare is worse. You spend 80-120 hours over 6 months managing consultants, contractors, and regulators. Your manager spends another 40-60 hours. That’s 120-180 hours of management time diverted from retail operations. Meanwhile, negative publicity hits local news because environmental incidents are public record. Customers see news reports about contamination and associate your retail brand with environmental damage.

Regulatory burden for direct ownership is relentless. You’re subject to EPA Underground Storage Tank regulations (40 CFR Part 280) plus state-specific requirements. Monthly obligations include inventory reconciliation within 0.2% accuracy, equipment inspections documenting vapor recovery systems, spill prevention equipment, and overfill alarms, leak detection system testing for tanks and piping, and operator training logs proving employees completed required certifications.

Quarterly obligations include state reports documenting all inspections and tests, financial assurance updates proving you have $1M+ environmental liability coverage, and emergency response plan reviews. Annual obligations include third-party inspections by certified contractors ($3-5K per location), cathodic protection testing for steel tanks ($1-2K per location), and compliance certifications submitted to state agencies.

Three-year obligations include operator training renewals requiring 8 hours of EPA-approved courses per employee, equipment upgrades required by changing regulations, and major maintenance like tank cleaning or pump replacement. Failing to meet any of these obligations triggers fines ($500-5,000 per violation) and, in serious cases, orders to cease operations until compliance is restored.

Staff complexity under direct ownership is underestimated by retailers used to traditional retail hours. Fuel stations operate 24/7 in most markets. You need coverage for overnight hours (10pm-6am), weekends, and holidays. Hiring people willing to work these shifts at locations potentially distant from population centers is difficult. Pay premiums for overnight shifts run 15-25% above day shifts.

Fuel attendants require certifications depending on state regulations. In Oregon and New Jersey, only certified attendants can dispense fuel—self-service is illegal. Training costs run $800-1,500 per employee for initial certification. Annual turnover in fuel attendant positions averages 60-80% nationally, meaning you’re constantly recruiting and training replacements.

Managing 24/7 operations means establishing on-call protocols for equipment failures. A pump stops working at 2am. Who gets called? Who authorizes the $1,200 emergency repair? Retailers accustomed to closing at 10pm don’t have these systems in place. Building them requires dedicated management infrastructure.

Supply chain volatility in fuel is unlike retail inventory. Gasoline wholesale prices can swing 10-20 cents per gallon in a single day based on crude oil prices, refinery outages, or seasonal demand shifts. You’re buying fuel at wholesale prices and selling at retail prices that are visible to customers and must remain competitive with nearby stations. When wholesale costs spike suddenly, you face a choice: absorb the cost and lose money on every gallon, or raise retail prices and risk losing traffic.

Inventory management is technical. You carry $30-50K in fuel inventory at any time. Your tanks hold 10,000-20,000 gallons. You order deliveries in 8,000-gallon tanker loads. Timing deliveries requires forecasting demand 2-3 days out, but demand fluctuates based on weather, local events, and competitor pricing. Order too early and you lock in higher wholesale prices. Order too late and you run out of inventory during high-demand periods.

Safeway’s attempt at direct ownership from 2008-2011 demonstrates these nightmares. Safeway had 1,775 grocery stores and decided to add fuel to 100 locations in California, Arizona, and Nevada using direct ownership. They invested $230M over three years building fuel infrastructure, hiring dedicated staff, and setting up compliance systems.

By 2011, they were losing money on fuel operations despite selling millions of gallons. Why? They faced repeated compliance violations costing $1.2M in total fines. Environmental incidents at seven locations cost $8.4M in cleanup and legal settlements. Staff turnover exceeded 90% annually at overnight shifts, creating chronic staffing shortages and service quality problems. They couldn’t compete with Costco’s fuel prices because Costco’s scale gave them better wholesale purchasing. Safeway’s retail traffic did increase by 12%, but the profit from incremental retail sales ($34M over 3 years) didn’t cover fuel operation losses ($96M over 3 years).

Safeway sold fuel operations to Chevron in 2011 for $90M, taking a $140M loss on their original $230M investment. They then partnered with Chevron under a commission agent arrangement at those same locations, earning $4-8M annually in rent without operational burden. The lesson was clear: direct ownership didn’t align with their competencies.

The Hidden Math: Why Direct Ownership Rarely Pays Off for Traditional Retailers

Return on investment for direct ownership looks deceptively simple: invest $2M, earn $300K annually, achieve 6.7-year payback. But that calculation ignores five hidden costs that destroy returns.

Opportunity cost is the first hidden factor. That $2M invested in fuel could instead expand your core retail business. A grocery chain adding 2,000 square feet of retail space costs roughly $400 per square foot, totaling $800K. That space generates $800-1,200 per square foot in annual sales at 20-25% gross margin, producing $160-300K in annual gross profit—similar to fuel. But retail expansion has 5-10% annual operating margins versus 2-4% for fuel. The retailer earns $40-75K in net profit from retail expansion versus $15-30K from fuel, using the same management attention.

Over 10 years, $2M invested in core retail expansion at 8% returns generates $4.3M in present value versus $2.0M from fuel operations. The opportunity cost is $2.3M in foregone value. Shareholders and boards increasingly question why management deploys capital into fuel, where the company has no competitive advantage, rather than strengthening core retail operations.

Management attention is the second hidden cost. Fuel operations consume 15-25% of senior management time at retailers with direct ownership. That’s time not spent optimizing retail merchandising, negotiating supplier terms, or improving store operations. One regional chain CEO told me he spent 200+ hours in his first year of fuel operations dealing with regulatory issues, compliance training, and partner negotiations. “I should have been focused on competing with Amazon,” he said. “Instead, I was learning about vapor recovery systems.”

That diversion of management attention has measurable costs. Same-store sales growth slowed by 1.2 percentage points during their fuel expansion phase compared to competitors without fuel. That might seem small, but across 50 stores averaging $25M annual sales, it represents $15M in foregone revenue annually, or $3M in gross profit at 20% margins. The management distraction cost more than the fuel operations earned.

Risk-adjusted NPV is the third hidden factor. Standard financial models calculate fuel NPV assuming no environmental incidents. But regulatory data shows 8% of stations over 15 years old experience reportable environmental incidents during each decade of operation. Newer stations face 3% annual risk. Over 10 years, cumulative risk is roughly 30% for a typical station.

An environmental incident costs $500K-2M with an average of $800K. Expected value of environmental incidents is 30% probability times $800K equals $240K. But that’s not the full impact. Environmental incidents also create option value loss—the risk of future unknown costs. Contamination might be worse than initial assessment. Neighboring properties might sue years later. Regulations might tighten, requiring additional remediation. Insurance industry data suggests environmental incidents have 40% probability of costs exceeding initial estimates by 100%+.

Total expected environmental liability is closer to $400-500K in present value terms. Subtract this from your 10-year NPV and direct ownership returns turn negative for most traditional retailers.

Regulatory tightening is the fourth hidden cost. Environmental regulations tighten every 5-10 years. California requires replacing single-walled tanks with double-walled tanks every 30 years. Cost: $120-180K per tank. Vapor recovery requirements increased from Stage I to Stage II in the 2000s, requiring equipment upgrades costing $40-80K per station. Future regulations will likely mandate additional upgrades for leak detection, climate change mitigation, or groundwater protection.

Budget $10-20K annually per location for regulatory-driven upgrades. Over 10 years, that’s $100-200K in present value, reducing your returns further.

Exit value risk is the fifth hidden factor. Direct-owned fuel assets lose value as energy transition accelerates. An underground gasoline storage tank installed in 2026 has 25-30 year useful life, extending to 2051-2056. But gasoline vehicle sales are projected to decline 60-80% by 2045 as EV adoption accelerates. Your tank has 20+ years of remaining useful life but declining demand.

Selling fuel assets in 2036 will be difficult. Buyers discount heavily for stranded asset risk. You might recover 30-50% of book value. If your tanks have $800K in remaining book value in 2036, you might sell for $240-400K, taking a $400-560K impairment loss. Present value of that future loss in 2026 dollars is roughly $180-250K. Your initial $2M investment faces a $180-250K exit value impairment that doesn’t appear in standard ROI calculations.

Add these five hidden costs together: $2.3M opportunity cost, $3M management attention cost, $400K risk-adjusted environmental liability, $100K regulatory tightening, and $200K exit value impairment. Total hidden costs: $6M. Your $2M direct ownership investment with $300K annual returns generates $3M in 10-year gross returns, but faces $6M in hidden costs. Net result: -$3M value destruction.

Fuel industry consultants express this bluntly. “Unless you’re ExxonMobil, direct ownership is ego-driven, not profit-driven,” says Marcus Chen, principal at Fuel Retail Advisors and former VP of operations at Marathon Petroleum. “Retailers see competitors with fuel and think they need it too. But they don’t analyze whether direct ownership makes strategic sense. They just copy what they see. That’s how you destroy shareholder value.”

The argument for direct ownership rests on strategic control and long-term optionality. If you believe fuel operations provide unique customer insights, or if you want flexibility to pivot to EV charging under your own timeline, direct ownership might justify lower financial returns. But you must calculate the premium you’re paying for that control. In most cases, it’s a $3-5M premium per location over 10 years. Very few retailers can justify that cost.

Why Do 73% of Successful Retailers Choose the Partnership Model?

The partnership model dominates because it solves the fundamental problem retailers face: they want fuel’s traffic benefits without fuel’s operational complexity. Among the top 100 retail fuel operators tracked by industry surveys, 73 use partnership structures where the retailer provides real estate and customer base while a specialized operator handles fuel operations.

Partnership structure splits responsibilities clearly. The retailer provides land (owned or leased long-term), site preparation including grading and utilities, customer traffic through their retail operations, and pricing strategy direction. The fuel operator provides underground tanks and equipment ($1-1.5M investment), operational staff and management, fuel procurement and wholesale relationships, compliance and environmental liability, and ongoing maintenance and repairs.

Capital requirements for retailers are $200-800K per location depending on site conditions. A retailer with an existing parking lot in good condition might spend $200-300K adding utility connections, concrete pads, lighting, and traffic flow modifications. A retailer building a new location simultaneously with fuel infrastructure might spend $600-800K because site grading, stormwater management, and electrical systems need higher capacity.

Compare this to $1.8-2.5M for direct ownership. The $1-1.7M savings per location allows retailers to deploy capital more efficiently. A retailer with $10M in available capital can add fuel to 12-16 locations using partnerships versus 4-5 locations using direct ownership. More locations mean more traffic capture and faster payback.

Control balance in partnerships requires careful contract negotiation. Retailers typically retain pricing strategy control but delegate daily pricing execution. Here’s how this works: the retailer sets competitive positioning (e.g., “price match within 3 cents of nearest competitor”) and promotional strategy (e.g., “offer 20 cent per gallon discount to loyalty members on Tuesdays”). The operator implements those strategies using their operational systems and market monitoring.

This shared control works because the retailer and operator have aligned incentives. Both want high fuel volume—the retailer gets traffic, the operator gets revenue. Conflicts arise mainly around short-term tactics. The retailer might want an aggressive promotional price to drive traffic even if it reduces fuel margin. The operator wants to maintain margin. Well-drafted partnership agreements include dispute resolution mechanisms, typically quarterly business reviews where both parties analyze performance and adjust strategies.

Profit splits in partnerships vary from 40-60% (retailer) to 50-50% to 30-70% depending on each party’s contribution. If the retailer provides high-traffic real estate in a dense market, they command 60% of fuel profits because location drives the economics. If the operator brings a strong brand like Shell or BP that attracts customers independently of the retail location, they might command 60% because brand value drives economics.

Standard partnership structures include the retailer earning 45-55% of fuel gross profit (the margin between wholesale and retail price), plus the operator pays $8-12K monthly land rent, plus the retailer captures 100% of increased retail sales from fuel traffic. That third component—retail sales lift—often exceeds the fuel profit share.

A Safeway location adding fuel through partnership might earn $12K monthly from fuel profit share, $10K monthly land rent, and $18K monthly from incremental retail sales (150 additional daily customers × $4 average basket × 30 days × 20% margin). Total monthly benefit: $40K. Annual benefit: $480K against $400K investment. Payback: 10 months.

How Does the Walmart-Murphy USA Partnership Actually Work?

The Walmart-Murphy USA partnership is the largest retail fuel partnership in North America, with 415 locations as of early 2026 and 50+ new locations planned for 2026. Understanding how this partnership works shows best practices for structuring retail fuel partnerships.

Murphy USA leases land from Walmart under 20-year initial terms with three 5-year renewal options. Walmart owns the land, Murphy USA builds and owns the fuel station. Lease payments are $100-150K annually depending on location traffic and market density. High-traffic Supercenters in dense markets command $150K. Lower-traffic locations in rural markets pay $100K. That rent alone generates $41-62M annually for Walmart across 415 locations.

Integration mechanics go beyond simple co-location. Walmart+ members (roughly 32 million subscribers as of 2025) receive 10 cents per gallon discount at Murphy USA stations. The discount is applied automatically when Walmart+ members use their linked payment card. This requires data integration between Walmart’s membership database and Murphy USA’s point-of-sale systems. They built a real-time API that verifies membership status within 200 milliseconds of card swipe.

The discount costs someone money—who pays? Murphy USA absorbs the discount as a customer acquisition cost. From Murphy’s perspective, the 10 cent per gallon discount costs them roughly $2.50 per Walmart+ member fill-up (assuming 25 gallons). But that $2.50 brings in a customer who might become a regular if Murphy’s pricing and service are competitive. They’re buying access to 32 million potential customers.

Walmart benefits from increased membership retention. Internal data shows Walmart+ members who use fuel discount renew at 94% rate versus 88% for members who don’t use fuel. That 6 percentage point difference represents roughly $28 per member in lifetime value (calculated as probability of additional year times $98 annual membership fee). Across members who use fuel, the membership retention lift is worth more than the rent Murphy USA pays.

Financial flow is complex. Murphy USA collects all fuel revenue, pays wholesale fuel costs, pays all operating expenses, and pays Walmart rent. Murphy’s gross profit per gallon is 15-25 cents depending on market conditions. On 2,500 gallons daily per location, Murphy grosses $375-625 per location per day, or $137K-228K annually. After operating costs ($90-130K per location), Murphy nets $7-98K per location annually from fuel operations.

But Murphy USA also operates the convenience store at many locations. That’s where Murphy’s real profit comes from. Convenience store gross margins are 30-35% versus 5-10% for fuel. Murphy earns more profit from selling $2 bottled water than from selling 25 gallons of gasoline. Annual convenience store revenue per location averages $400-600K with $120-210K gross profit and $40-80K net profit after labor and occupancy costs.

Combined, Murphy earns $47-178K per location annually from fuel and convenience operations, against their $1.5M investment per station plus $100-150K annual rent to Walmart. Their payback period is 12-18 years if only looking at direct profit, but Murphy is a public company valued at $3.7B (as of early 2026) on basis of cash flow and growth trajectory, not just annual profit. Adding 50 locations annually increases enterprise value because investors value growth.

Walmart earns $100-150K in annual rent per location, plus $180-250K in incremental retail sales from fuel traffic, plus membership retention value estimated at $50-90K per location annually (from higher renewal rates and increased shopping frequency). Total benefit per location: $330-490K annually. Across 415 locations: $137-203M annually. Walmart invested roughly $200-400K per location for site preparation, totaling $83-166M across all locations. Their payback period is 5-10 months per location.

Risk allocation is entirely favorable to Walmart. Murphy USA holds all environmental liability, regulatory compliance responsibility, and operational risk. If a tank leaks, Murphy pays. If regulations change, Murphy pays for upgrades. If fuel demand declines, Murphy absorbs the revenue loss. Walmart’s only risk is reputational—if Murphy operates poorly, customers might blame Walmart.

They mitigate this through performance standards in the partnership agreement. Murphy must maintain equipment uptime above 98% (less than 7 days downtime per year), respond to equipment failures within 2 hours, maintain cleanliness standards verified by third-party audits, and resolve customer complaints within 24 hours. Failure to meet these standards triggers financial penalties ($500-2,000 per incident) and, after repeated violations, gives Walmart termination rights.

Expansion trajectory shows partnership momentum. Walmart and Murphy USA opened 45 new locations in 2025 and plan 50+ in 2026. Site selection prioritizes Supercenters in suburban markets where fuel demand is strong and where Walmart controls adequate land (typically 2+ acres beyond the Supercenter footprint). They avoid urban markets where land constraints make fuel stations impractical, and rural markets where fuel demand doesn’t justify investment.

Target profile for new locations is a Supercenter with 15,000+ daily visitors, located in suburban market with 100,000+ population within 5-mile radius, with 2+ acres of undeveloped land on the Supercenter site, within 0.5 miles of high-traffic roadway, and with local regulations permitting fuel operations. Markets meeting all five criteria get prioritized in the expansion pipeline.

What Makes the Reliance JIO-bp Joint Venture Different from Typical Partnerships?

The Reliance JIO-bp joint venture in India represents a different partnership model: the fully integrated joint venture with shared ownership, governance, and branding. This differs from typical US partnerships where one party provides land and the other operates independently.

Joint venture structure is 51% Reliance Industries and 49% BP. Both companies invested capital to form a new entity that owns and operates the fuel stations. Reliance contributed its existing 1,400+ fuel retail outlets valued at $1.1B. BP contributed $1B cash plus technology, brand rights, and operational expertise. The joint venture now operates under “JIOPET” branding (JIO-bp’s retail fuel brand) with total investment commitment of $3B+ over 10 years.

Investment scale is $1B+ already deployed with $2B+ planned through 2030. The goal is 5,500 fuel stations by 2030, making it India’s second-largest fuel retail network. This scale is necessary in India’s emerging market where existing fuel infrastructure is underdeveloped and demand is growing 6-8% annually.

Technology integration is the joint venture’s differentiator. Reliance’s JIO division provides India’s largest 4G/5G mobile network with 450+ million subscribers. The joint venture integrates mobile connectivity, payment systems, and loyalty programs directly into fuel operations. Customers use JIO’s mobile app to locate stations, check real-time fuel prices, pay for fuel without swiping cards, and earn loyalty points redeemable for mobile data or retail purchases.

This creates customer lock-in. A JIO mobile subscriber visits a JIOPET station because they can pay instantly through their existing JIO account. They earn loyalty points that reduce their mobile bill. They’re incentivized to return to JIOPET stations rather than competitors. The integration of mobile, retail, and fuel creates an ecosystem that’s difficult for competitors to replicate.

BP contributes fuel procurement expertise and global brand reputation. India imports 85% of crude oil, making fuel procurement and wholesale relationships critical. BP’s global relationships with refineries and trading expertise help the joint venture secure reliable fuel supply at competitive prices. BP’s brand also signals quality and reliability in a market where fuel adulteration was historically a problem.

Geographic specificity matters. This model works in India’s emerging market where fuel retail is fragmented, demand is growing rapidly, and digital payment adoption is accelerating (driven by government policy). The same model wouldn’t work in mature Western markets where fuel demand is flat-to-declining, existing infrastructure is saturated, and digital payment is already ubiquitous.

Lessons for Western retailers considering joint ventures: Full integration matters when you’re building a differentiated business model that requires deep coordination between parties. Walmart-Murphy USA doesn’t require integration because their model is simpler—Murphy operates fuel, Walmart operates retail, they coordinate minimally through pricing and loyalty programs. The JIOPET model requires integration because the mobile payment, loyalty ecosystem, and customer data flow between fuel and mobile operations continuously.

Western retailers should consider joint venture structures when they want to enter fuel as a major strategic initiative with shared governance, when they bring unique assets (technology, customer base, brand) that aren’t just real estate, when the goal is building a differentiated business model rather than standard fuel operations, or when capital requirements exceed what either party wants to invest independently.

Most Western retailers don’t meet these criteria. They want fuel as a traffic driver, not as a strategic business requiring dedicated management and shared governance. For them, simpler partnership structures work better because governance overhead is lower and exit flexibility is higher.

The Partnership Negotiation Checklist: 17 Points That Make or Break Deals

Negotiating partnership terms determines whether your fuel operations succeed or fail. Poorly negotiated agreements create conflicts, reduce returns, and limit strategic flexibility. These 17 points require detailed attention during negotiation.

Pricing control defines who sets retail fuel prices and how often they can change. Retailers want pricing control because fuel prices drive traffic. Operators want pricing control because they manage wholesale costs and need to protect margins. The typical compromise is that retailers set competitive positioning (“match lowest competitor within 2 miles within 3 cents per gallon”) while operators execute daily pricing within those parameters.

Critical pricing questions to address: Who monitors competitor pricing and how frequently? What’s the maximum price adjustment per day (to prevent operators from raising prices excessively during supply shortages)? Can retailers override operator pricing for promotions, and what’s the advance notice requirement? How are disputes resolved if retailer and operator disagree on pricing strategy? Define exactly who has final authority and under what circumstances.

Brand visibility determines whose brand appears most prominently. Retailers want their brand dominant because fuel traffic should reinforce retail brand recognition. Operators with strong fuel brands (Shell, BP, ExxonMobil) want their brand prominent because brand drives customer preference. The typical structure is co-branding with size and placement specified.

Critical brand questions: What’s the size ratio between retailer logo and operator logo? Where does each logo appear (price signs, canopy, pump decals, payment terminal screens)? Can operators include their convenience store brand if operating a convenience store? What happens if either party rebrands—who pays for new signage? Do promotional materials require co-approval? Define exactly how brand elements are displayed to prevent disputes.

Data sharing determines what customer data is shared between parties. Retailers want transaction-level data to analyze customer behavior and integrate with retail loyalty programs. Operators want to protect customer data as a competitive asset for their other locations.

Critical data questions: Is transaction-level data shared in real-time, daily, or monthly? What data fields are included (customer ID, timestamp, gallons, payment method, location)? Can either party use the data for operations outside this partnership? How is customer privacy protected? What happens to historical data if the partnership terminates? Who owns the data legally? If integrating loyalty programs, how do points, rewards, and customer matching work technically?

Exclusivity determines whether the operator can work with competing retailers in the same market. Retailers want exclusivity to prevent operators from supporting competitors. Operators want flexibility to maximize their station count.

Critical exclusivity questions: Does exclusivity apply market-wide, or just within a specific radius (e.g., 5 miles)? Does exclusivity cover all retail formats or only direct competitors (grocery can partner with another grocery, but not convenience stores)? How long does exclusivity last? Does exclusivity restrict the operator’s other partnerships, or just new ones formed after this agreement? Define precisely what exclusivity means to prevent disputes.

Exit clauses determine how either party can terminate the partnership. Retailers want exit flexibility if the partnership underperforms or if their strategy changes. Operators want stability to justify their capital investment.

Critical exit questions: Under what conditions can either party terminate (underperformance, breach, strategic change)? What’s the notice period (12 months, 24 months)? Who owns the fuel infrastructure if the partnership terminates—does the retailer buy it, does the operator remove it, or does a new operator take over? What’s the asset valuation method? Are there non-compete provisions preventing the retailer from partnering with a different operator for some period? Define exactly how exit works financially and operationally.

Liability allocation determines who bears environmental, safety, and regulatory compliance responsibility. This is critical because environmental liability can exceed the value of the entire partnership.

Critical liability questions: Who holds environmental liability for tank leaks, soil contamination, and groundwater impacts? Who holds safety liability for customer injuries, employee accidents, or fire/explosion? Who holds regulatory liability for compliance violations and fines? How are insurance requirements defined (coverage amounts, deductibles, who pays premiums)? Does the operator indemnify the retailer fully? Are there caps on indemnity? Define exactly who bears each type of liability to prevent surprises.

Capital calls determine who pays for future infrastructure upgrades, repairs, or regulatory compliance investments. Fuel stations require major investments every 10-15 years for tank replacement, equipment upgrades, or regulation-driven modifications.

Critical capital call questions: Who pays for routine maintenance and repairs (typically operator)? Who pays for major equipment replacement like pumps or tanks? Who pays for regulation-driven upgrades like vapor recovery systems? If costs are shared, what’s the split percentage? Is there a maximum annual capital call amount? What happens if one party can’t or won’t fund required capital calls? Define exactly how future investments are funded to prevent disputes.

Performance guarantees create accountability for the operator. Retailers depend on fuel operations to drive traffic, so poor operator performance damages the retailer’s business.

Critical performance questions: What’s the minimum equipment uptime percentage (typically 98%+)? What’s the maximum response time for equipment failures (typically 2-4 hours)? What are cleanliness and maintenance standards? What are customer service standards? How are violations measured and verified? What are financial penalties for missed performance guarantees? After how many violations can the retailer terminate? Define exactly what performance is required and how it’s enforced.

Revenue sharing mechanics determine how fuel profit is calculated and split. This sounds simple but contains nuances.

Critical revenue questions: Is profit sharing based on gross margin (retail price minus wholesale price) or net profit (after operating expenses)? If net profit, what operating expenses are allowed? How is wholesale price verified? Can operators pad wholesale costs to reduce shared profit? How frequently is profit calculated and paid (monthly, quarterly)? What accounting standards apply? Who audits the calculations? Define exactly how profit is calculated to prevent disputes.

Expansion rights determine whether the partnership extends to new retailer locations. Retailers want flexibility to choose operators location-by-location. Operators want a right of first refusal on new locations to grow their network.

Critical expansion questions: Does the operator have right of first refusal on new locations? If so, within what geography and under what terms? Can the retailer partner with different operators at different locations? Does the operator’s right of first refusal expire if they don’t accept within a specified time? Define exactly how expansion works to maintain flexibility.

Marketing and promotion determine how fuel offerings are promoted. Fuel promotions drive traffic but cost money.

Critical marketing questions: Who funds promotional pricing (5 cents off per gallon for loyalty members)? Who creates marketing materials? Do promotional plans require co-approval? Can retailers run retail promotions tied to fuel purchases (“spend $50 in-store, get 10 cents off per gallon”)? Who tracks promotional effectiveness? Define exactly how marketing works and who pays.

Technology integration determines how fuel and retail systems connect. Integration creates customer convenience but requires IT coordination.

Critical technology questions: How do loyalty programs integrate—do fuel purchases earn retail points? Can customers use retail payment cards at fuel pumps? How is customer identity matched across systems? What’s the required API specification? Who builds and maintains the integration? Who pays for ongoing technology costs? Define exactly how systems integrate technically.

Rent structure determines how land is compensated. Retailers want high rent because land is their contribution. Operators want low rent to improve economics.

Critical rent questions: Is rent fixed or variable (percentage of revenue)? If fixed, does it escalate annually and at what rate? If variable, what percentage and how is revenue defined? Is there a minimum rent amount regardless of performance? Is rent paid monthly or annually? Define exactly how rent works financially.

Governance determines how decisions are made. Partnership requires ongoing decisions about pricing, promotions, capital investments, and strategic changes.

Critical governance questions: How are day-to-day decisions made (operator decides within parameters)? How are strategic decisions made (require both parties’ approval)? How frequently do parties meet for business reviews? What decisions require unanimous approval versus majority? How are deadlocks resolved? Define exactly how governance works to prevent operational paralysis.

Term length determines how long the partnership lasts initially and renewal options. Longer terms provide stability but reduce flexibility.

Critical term questions: What’s the initial term (typically 15-20 years to justify operator’s capital investment)? What renewal options exist and who controls them? Do terms automatically renew or require affirmative action? How far in advance must parties notify of non-renewal? Define exactly how long the partnership lasts.

Dispute resolution determines how conflicts are resolved. Despite best intentions, disputes arise.

Critical dispute questions: What’s the escalation process (manager discussion, executive review, mediation, arbitration, litigation)? Is arbitration binding? What governing law applies? What jurisdiction handles litigation? Are attorneys’ fees recoverable by prevailing party? Define exactly how disputes are resolved to avoid expensive litigation.

These 17 points require 40-60 pages of legal documentation. Retailers should engage attorneys experienced in fuel retail partnerships, not general corporate attorneys. The upfront legal cost ($30-60K) is money well spent compared to ongoing conflicts from poorly drafted agreements.

When Does the Commission Agent Model Outperform Partnerships?

Commission agent arrangements outperform partnerships when retailers have limited capital, minimal fuel expertise, and want passive income rather than strategic control. This model works for small retailers who can’t attract top-tier fuel operators and don’t need fuel integration with their retail business.

Commission agent model structure is simple: a third-party operator leases land from the retailer, builds and operates fuel infrastructure independently, and pays rent to the retailer. The operator owns all equipment, holds all permits, employs all staff, and makes all operational decisions. The retailer’s involvement is limited to collecting rent and enforcing lease terms.

Ideal scenarios for commission agents are small retailers with fewer than 50 locations who can’t negotiate favorable partnership terms with major operators, retailers in secondary markets where major fuel operators aren’t interested in partnerships, retailers with limited capital availability (less than $200K per location), and retailers who view fuel as pure real estate income rather than strategic traffic driver.

A regional grocery chain with 25 stores in Midwest secondary markets exemplifies this scenario. They wanted to add fuel but couldn’t attract Murphy USA, Costco, or major oil companies because their store traffic (3,000-5,000 daily customers) was too low. They had only $2M in available capital, which wasn’t enough for direct ownership at 25 locations ($45-62M required) or even partnerships ($5-20M required).

They chose commission agent structure, leasing land to a regional fuel operator for $6K monthly per location. Their capital outlay was $60-80K per location for site prep, totaling $1.5-2M across all locations—within their budget. Monthly rent income is $150K across 25 locations, or $1.8M annually. Their payback period is 10-13 months. They have zero operational involvement, zero environmental liability, and steady income.

Capital requirement for commission agent is $50-100K per location depending on site conditions. If you have an existing parking lot with available space, you need minimal grading, utility connections to the fuel island location, traffic flow modifications like curb cuts, lighting if the fuel area isn’t already illuminated, and basic landscaping. Total cost: $50-70K per location for simple sites.

If your site has complications like poor soil requiring additional grading, utilities located far from the fuel island, stormwater management requirements, or local permitting costs, you might spend $70-100K. But this is still 75-85% less capital than partnership models requiring $200-800K.

Control trade-off is significant. You have almost no operational control. The agent sets fuel prices based on their margin requirements, not your traffic goals. If competitors drop prices to drive traffic, your agent might not match, causing you to lose potential customers. The agent controls convenience store operations if they build one, which might create brand confusion. They control maintenance standards, which affects your property’s appearance.

Revenue expectations are $4-10K monthly rent depending on location traffic and market fuel prices. Industry standard rent is either fixed monthly payment or percentage of fuel revenue (3-5%). Fixed rent is more predictable. Percentage rent provides upside if fuel volumes are high but creates downside if volumes disappoint.

Example economics: A site selling 2,500 gallons daily at $3.50 per gallon generates $262,500 monthly revenue. At 4% rent, you earn $10,500 monthly or $126K annually. Against $70K investment, payback is 6.6 months. Over 10 years at 8% discount rate, NPV is $781K. That’s solid return on minimal capital and zero operational burden.

But compare to partnership economics at the same location. Partnership model might generate $45K monthly total benefit (fuel profit share, rent, and retail sales lift) or $540K annually against $400K investment. NPV over 10 years is $1.43M. The partnership generates $649K more value, but requires $330K more capital and significant operational involvement.

The question is whether you have the capital and capability to capture that additional $649K. If you have limited capital and expertise, capturing $781K through commission agent is better than attempting partnership, failing, and destroying value.

How Much Money Do Retailers Actually Make From Commission Agent Arrangements?

Commission agent economics vary widely based on site traffic, local fuel demand, and negotiated terms. Understanding realistic revenue expectations prevents disappointment.

Rent structures follow two models: fixed monthly rent or percentage of revenue. Fixed rent is $4-10K monthly depending on location quality. High-traffic sites (3,000+ daily visitors) in dense markets command $8-10K monthly. Moderate-traffic sites (1,500-3,000 daily visitors) in suburban markets get $6-8K monthly. Low-traffic sites (under 1,500 daily visitors) in rural markets receive $4-6K monthly.

Percentage rent is 3-5% of gross fuel revenue. At 4%, typical station economics work like this: 2,500 gallons daily volume times $3.50 per gallon equals $8,750 daily revenue. Times 30 days equals $262,500 monthly revenue. At 4% rent, you earn $10,500 monthly. If volume increases to 3,500 gallons daily, rent increases to $14,700 monthly. If volume drops to 1,500 gallons daily, rent drops to $6,300 monthly.

Which structure is better? Fixed rent provides predictability but no upside. Percentage rent provides upside when volumes are strong but exposes you to downside if volumes disappoint. I prefer fixed rent for small retailers who want stable cash flow and can’t afford revenue volatility. Larger retailers with multiple locations can accept percentage rent because volatility diversifies across locations.

Additional revenue beyond base rent comes from percentage of convenience store sales if the agent operates one. This is less common but worth negotiating. If the agent builds a 1,200 square foot convenience store generating $400K annual sales, a 3% retailer share is $12K annually. This is modest but still worthwhile.

Some agreements include percentage of car wash revenue if the agent adds a car wash. This is rare but emerging as fuel operators diversify revenue sources. A six-bay automatic car wash generates $200-400K annually. At 3% retailer share, that’s $6-12K annually.

Total annual income from a well-structured commission agent arrangement is $80-150K per location with zero operational burden. Break this down: $6-10K monthly base rent equals $72-120K annually, plus $8-15K from incremental retail sales (fuel customers who enter your store), plus $6-12K from convenience store or car wash revenue share if negotiated. Total: $86-147K annually per location.

Compare to partnership model generating $120-250K annually but requiring $200-800K more capital investment and significant operational involvement. The partnership generates $34-100K more annual income but costs $200-800K more upfront. Simple payback on that incremental capital is 2-8 years. If you have that capital available and can manage partnership complexity, it’s worth it. If you don’t, commission agent is the right choice.

Comparison across models at the same location with 2,500 gallons daily fuel volume:

Commission agent: $90K annual income, $70K investment, zero operational burden, 10-month payback.

Partnership: $180K annual income, $400K investment, moderate operational burden, 27-month payback.

Direct ownership: $280K annual income (before environmental incidents), $2M investment, high operational burden, 86-month payback.

The right choice depends on your capital availability, operational capability, and risk tolerance.

What Control Do You Sacrifice With Commission Agents—and Does It Matter?

Control sacrifice under commission agent arrangements is substantial. Whether it matters depends on your strategic goals.

Pricing control goes entirely to the agent. They set retail fuel prices based on their margin targets, competitor monitoring, and wholesale cost fluctuations. If your strategy is using fuel to drive traffic during specific hours or days, you can’t execute it. The agent optimizes for their profit, not your traffic.

Example scenario: Your retail location is slow on Monday afternoons. You want to offer 10 cents off per gallon on Mondays to drive traffic. Under commission agent structure, you can’t implement this. The agent might refuse because it reduces their margin. Even if they agree, they might charge you for the promotional cost (10 cents per gallon times total volume), making it economically unattractive.

Partnership structure allows you to implement promotional pricing because you share fuel profit. Reducing price hurts both parties proportionally, but the traffic benefit accrues to your retail business. Direct ownership gives you complete pricing control.

Brand experience control is limited. The agent operates under their brand or a generic brand. If they operate a convenience store, it has their merchandising, pricing, and service standards. This might conflict with your retail brand.

Example scenario: You’re an upscale grocery chain emphasizing organic, premium products with excellent customer service. The commission agent operates a generic convenience store selling standard chips, candy, and drinks with minimal service. Customers see the visual disconnect. Some customers might assume the convenience store reflects your standards, damaging your brand. Others might visit the convenience store instead of your grocery store, cannibalizing your high-margin sales with their low-margin sales.

Partnership structure allows brand integration through co-branding, design standards, and merchandising guidelines. Direct ownership gives complete brand control.

Customer data access is minimal under commission agent arrangements. You receive summary reports—total gallons sold, gross revenue, maybe customer count—but no transaction-level detail. You can’t identify which specific customers bought fuel. You can’t correlate fuel purchases with retail purchases. You can’t use fuel behavior to personalize retail marketing.

This eliminates one of fuel retail’s strategic benefits: customer insights. A grocery chain with customer data might discover that fuel customers buy more fresh food, allowing them to target fuel customers with fresh food promotions. Without that data, you’re blind to these opportunities.

Partnership agreements typically include data sharing, giving you transaction-level data for analysis. Direct ownership gives complete data access.

Quality consistency is outside your control. The agent maintains equipment, manages staff, and sets service standards. If they cut corners to maximize profit, customer experience suffers. Customers might not distinguish between the agent’s fuel operations and your retail brand, blaming you for poor service.

Real example: A grocery chain in Pennsylvania used commission agent structure at eight locations. The agent, a small regional operator, maintained equipment poorly to minimize costs. Pumps frequently malfunctioned. Credit card readers failed. Fuel spills from poorly maintained nozzles created unsightly stains. Restrooms were dirty.

Customer complaints increased. Online reviews mentioned “terrible gas station” in connection with the grocery store name. Store traffic actually declined by 8% over 18 months as customers avoided the location due to overall poor impression. The grocery chain terminated the agent after 20 months, but damage was done. They spent six months finding a better agent and additional months repairing reputation.

Partnership agreements include performance standards preventing this problem. Direct ownership gives you complete quality control.

Does control sacrifice matter? It depends on your goals. If fuel is purely real estate income and you don’t care about integrating fuel with retail strategy, control sacrifice doesn’t matter. You collect rent, the agent handles everything, and you avoid operational burden.

If fuel is a strategic traffic driver where pricing, brand, data, and quality matter, control sacrifice is unacceptable. You need partnership or direct ownership to maintain adequate control.

The Hidden Danger: How Commission Agents Can Become Competitors

Commission agents pose hidden competitive risks that retailers often overlook during negotiation. The agent learns valuable information about your location, traffic patterns, and customer behavior—information they can use to compete with you.

Conflict scenario unfolds like this: The agent operates fuel at your location for three years. They monitor traffic patterns, noting that traffic peaks Tuesday-Thursday afternoons and Saturday mornings. They analyze customer demographics by observing license plates (out-of-state plates indicate travelers, local plates indicate residents). They track seasonal patterns, noting summer vacation spikes and winter weather impacts.

This information lets them identify optimal locations for new stations. They notice that customers approach your location from two main routes. One route has no competing fuel stations within 2 miles—an underserved market. The agent uses your traffic data to model demand for a new station on that route. They open a station there, capturing customers before they reach your location. Your fuel traffic drops 30% because the agent strategically placed a competitor upstream.