How Budget Planning Helps Businesses Avoid Financial Stress

Budget planning isn’t about making perfect spreadsheets. It’s about knowing exactly when you’ll hit zero and what you’ll do before that happens. I’m going to show you how real businesses—agencies, e-commerce stores, SaaS startups, restaurants—use actual planning frameworks to survive the first brutal year.

No theory. Just numbers that either worked or killed the business.

The Thing That Kills Most Businesses First

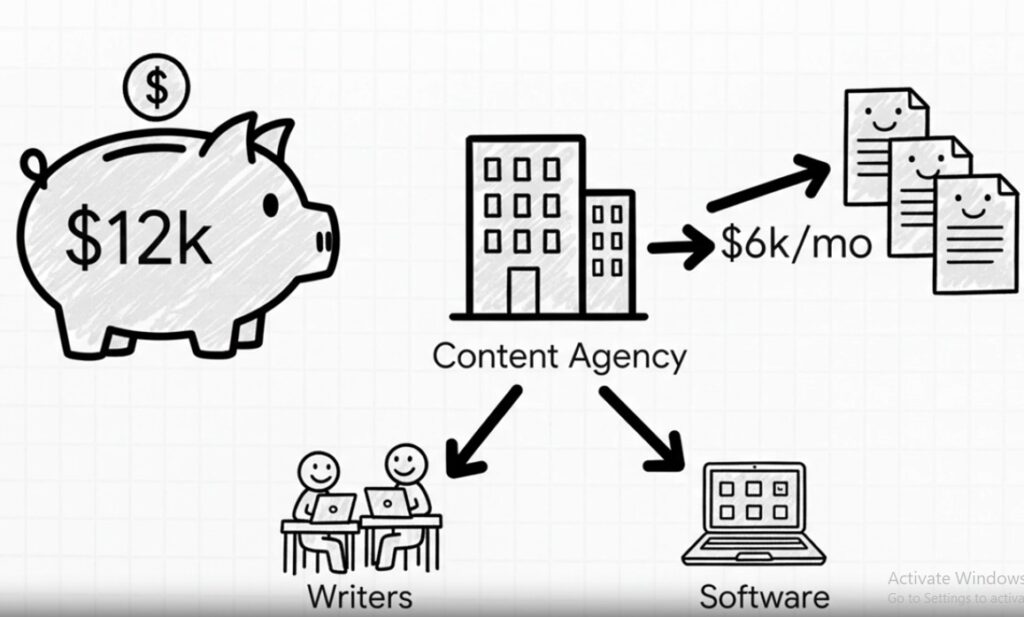

Here’s what happens when you launch a content writing agency with $12,000 saved.

You sign three clients in week one. They’re each paying $2,000 monthly. You’re thrilled. On paper, you’re making $6,000 a month with $12,000 in the bank. You hire two freelance writers immediately. You buy the premium tools. Website hosting, Grammarly Premium, project management software, Google Workspace.

You’re dead broke by month four.

Why? Because you paid weekly but got paid monthly. Your clients were on NET-30 terms, which means you did work in March, invoiced at month-end, and got paid in early May. Meanwhile, you paid those two freelance writers every two weeks. You paid for all your tools immediately.

The actual math looks like this:

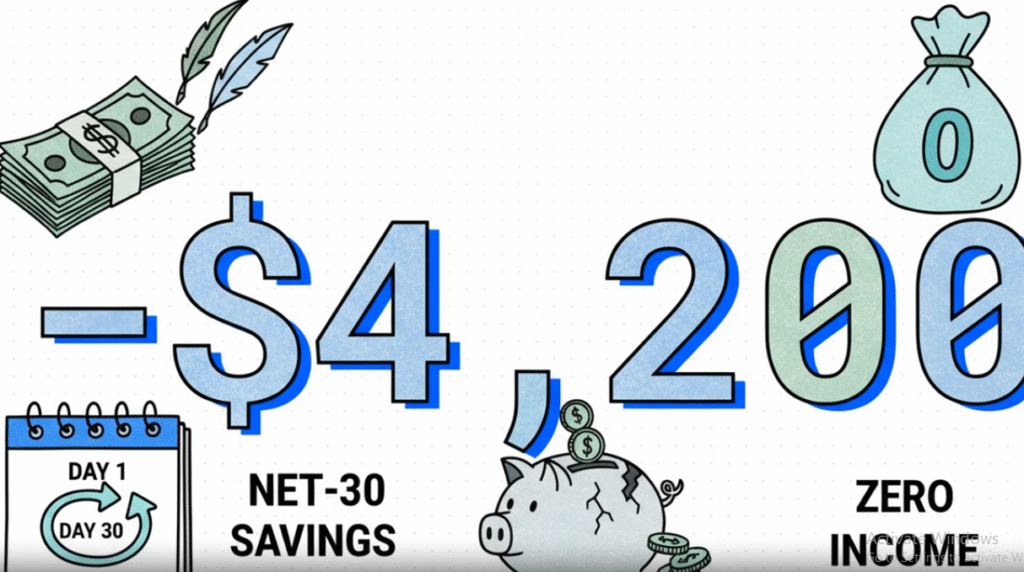

Month 1 – Spent $4,200 on writers and tools, earned $0 Month 2 – Spent $4,200, earned $0 Month 3 – Spent $4,200, earned $6,000 (first payment finally arrives)

By month two, you’d burned through $8,400 of your $12,000. You still have bills of $4,200 but only $3,600 left. So you put it on a credit card. By month four, you’re paying 22% interest on $3,800 of debt even though you’re “profitable.”

The planned version looks completely different.

Before launching anything, you map cash flow week by week, not month by month. Service businesses pay weekly but get paid monthly. Your planning has to account for that gap, or you’re finished before you start.

With $12,000 and monthly costs of $4,200, you need minimum $16,800 to survive the first 90 days. That’s $4,200 times four months, minus the $6,000 that finally arrives in month three. You’re $4,800 short.

So you have three actual options. Delay launch until you save $17,000. Start with one writer instead of two, which cuts monthly costs to $2,600. Or negotiate upfront deposits with clients—50% before work starts.

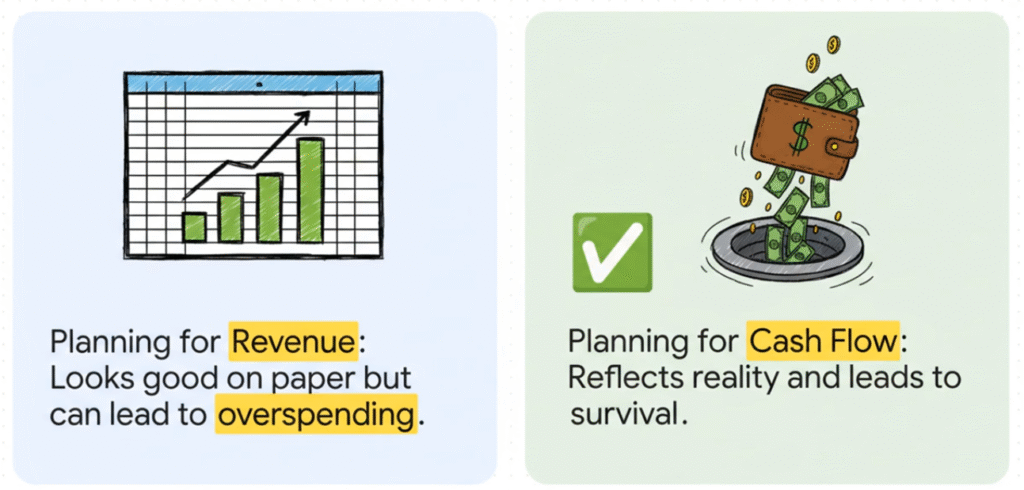

Most people do none of these because they never planned cash flow. They planned revenue. That’s the difference between surviving and closing.

If You’re Starting a Digital Marketing Agency

Let’s say you want to launch a digital marketing agency but you can’t afford an office or full-time team. You’ve saved $8,000. Here’s the month-by-month plan that actually works.

The first three months are about validation, not profit.

You’re not guessing what services to offer. You’re testing with minimum investment.

Month one expenses:

- Domain and professional email through Google Workspace: $12

- Website on Webflow: $23

- Calendly for scheduling: $10

- Canva Pro for designs: $13

- LinkedIn Sales Navigator for outreach: $80

- Emergency buffer: $150

Total monthly overhead is $288. Notice what’s missing—no office, no employees, no fancy software. You’re doing everything yourself.

Your outreach pitch has to be specific and measurable. “I’ll run your Google Ads for 30 days. You pay only the ad spend. If I don’t get you 10 qualified leads, the management is free.” You’re not selling time. You’re selling an outcome.

In month one, you close zero clients. You spent $288 and made $0.

Month two, you close one client—a local HVAC company. They agree to $1,500 ad spend plus $500 management fee if you hit the lead target.

Your actual math for month two:

- Revenue: $0 (client pays at end of month after results)

- Expenses: $288

- Bank balance: $8,000 minus $288 minus $288 equals $7,424

Month three is where things shift. The HVAC client got 14 leads. They paid the $500 and renewed. You closed two more clients using that case study—a dental clinic and a roofing company, same deal structure.

Month three financials show revenue received of $500 from the HVAC client. Revenue pending is $1,500 from three clients at $500 each, which gets paid in month four. Expenses stay at $288. Your bank balance is now $7,636.

You’re barely cash-flow positive. Most people panic here.

But if you planned this right, your goal for months one through three was never profit. It was proof. You need three case studies with real numbers before you can scale anything.

Months four through six are about leveraging freelancers without going broke.

By month four, you’ve got three active clients and case studies showing 12 to 15 leads per client monthly. Now you can scale, but you still can’t afford full-time people.

Your new expense structure adds a freelance ad specialist at 20 hours monthly for $25 an hour, which is $500. You add a freelance copywriter at 15 hours monthly for $30 an hour, another $450.

New monthly burn rate is $1,238.

But your pricing changes too. With proof of results, you’re not charging $500 anymore. You’re charging $1,200 monthly for ad management plus 10% of ad spend as your commission.

Month four breakdown looks like this:

The HVAC client spends $1,500 on ads. You earn $150 commission plus $1,200 management, total $1,350.

The dental client spends $2,000 on ads. You earn $200 commission plus $1,200, total $1,400.

The roofing client spends $1,200 on ads. You earn $120 plus $1,200, total $1,320.

Month four revenue is $4,070. Expenses are $1,238. Profit is $2,832.

Your bank balance is now $10,468.

Here’s where most people mess up. They see $2,832 profit and think they can afford an office or hire someone full-time. Don’t.

Months four through six are your test phase for freelancers. The question you’re answering is: can I delegate ad management? Can I focus only on sales and strategy? Can I scale revenue faster than I scale costs?

In month five, you add two more clients using the same outreach method. Revenue jumps to $6,700. Expenses go to $1,688 because you’re giving the ad specialist more hours. Profit is $5,012.

Month six, you’ve got seven clients. Revenue is $9,450. Expenses are $2,100 because both freelancers are now part-time. Profit is $7,350.

At the end of month six, your bank balance is $25,662. Here’s what the budget plan tells you—you now have enough cash to survive 12 months even if every client cancels tomorrow. That’s $2,100 times 12 equals $25,200.

That’s your safety threshold. That’s when you know you’re actually stable.

The office decision happens in months seven through nine, and most people get it completely wrong.

Agency owners get an office because they feel successful. That’s ego, not planning.

The question is: will an office increase revenue or just increase expenses?

Your current client meetings are all on Zoom. None of your seven clients have ever asked to meet in person. Your freelancers work remotely and prefer it. An office in a shared workspace would cost $800 monthly for rent, $150 for utilities and internet, $100 for coffee and supplies.

That’s $1,050 monthly, which is $12,600 annually for something that won’t increase revenue.

So you skip it.

Instead, you invest in sales infrastructure. You hire a part-time sales VA for $600 monthly to handle lead qualification. You upgrade to HubSpot CRM at $450 monthly to track your pipeline. You start running LinkedIn ads to generate inbound leads at $800 monthly ad spend.

New expenses are $1,850 monthly added to your existing costs.

Month seven financials show revenue of $11,200 from nine clients now. Expenses are $2,100 for freelancers plus $1,850 for sales infrastructure, total $3,950. Profit is $7,250.

The sales infrastructure works. By month nine, you’ve got 14 clients and you’re turning people away. Revenue is $18,900. Expenses are $4,200 because you increased freelancer hours. Profit is $14,700.

Bank balance at end of month nine: $60,012.

Months ten through twelve are when you transition from freelancers to actual employees.

You’ve got a real problem now. Your freelancers are maxed out. The ad specialist is working 35 hours weekly—basically full-time but still a contractor. The copywriter is at 30 hours weekly. If you want to grow past 14 clients, you need full-time people.

Here’s the budget planning calculation that most people skip:

Option one is keep freelancers and cap growth at 14 clients. Revenue stays at $18,900 monthly. Expenses stay at $4,200 monthly. Profit is $14,700 monthly, which is $176,400 annually.

Option two is hire two full-time employees and scale to 25 clients.

Full-time employee costs break down like this:

- Junior ad specialist at $3,500 monthly ($42,000 annual salary)

- Junior copywriter at $3,200 monthly ($38,400 annual salary)

- Payroll taxes at 15% add $1,005 monthly

- Basic health insurance adds $600 monthly

- Software and tools add $500 monthly

Your new monthly employee costs are $8,805.

To break even with your current profit of $14,700, you need revenue of $8,805 plus $4,200 in other expenses, which equals $13,005.

You’re already making $18,900, so you’re safe on paper. But here’s the actual plan—you need to grow to 20 clients before hiring. Why?

If you hire at 14 clients and lose three clients in a bad month, your revenue drops to $14,850. That barely covers your new $13,005 in expenses. You’ve got no safety margin.

The rule is simple: your revenue should be 1.5 times your expenses before hiring full-time.

You need $13,005 times 1.5, which equals $19,508 in monthly revenue. That’s about 15 clients at your average rate.

In month ten, you focus purely on sales. You close four more clients for a total of 18. Revenue hits $23,400.

Month ten checkpoint shows revenue of $23,400, expenses of $4,200, profit of $19,200. Bank balance is now $79,212.

Now you’re ready.

In month eleven, you make the first hire—one full-time ad specialist. You keep the copywriter as a freelancer for now.

Month eleven expenses break down to $2,100 for freelancers (just the copywriter now), $4,105 for the full-time ad specialist including salary, taxes, and insurance, $1,850 for sales infrastructure, and $288 for basic overhead. Total is $8,343.

Revenue stays at $23,400. Profit drops to $15,057, but it’s still healthy.

In month twelve, you hit 22 clients. Revenue is $28,600. You hire the second full-time employee, the copywriter. Your new monthly expenses are $12,148.

Month twelve profit is $16,452.

Year-end bank balance: $110,721.

Now the office decision looks different. With two full-time employees, an office might make sense. But you don’t rush it. Your plan for year two is to keep the team remote for months one through three, which saves $3,150 in office rent. In month four, you get a small office only if the team requests it. You use that $3,150 in savings to upgrade software and tools instead.

That’s disciplined planning.

If You’re Launching an E-Commerce Store

E-commerce is different. The mistake here is spending everything on inventory upfront.

Let’s say you want to sell handmade candles online. You’ve saved $5,000. The tempting logic is to buy materials in bulk and save 30% per unit. You could make 200 candles for $3,200 instead of $4,500.

Here’s what actually happens. You spend $3,200 on inventory upfront. You sell 18 candles in month one. You’ve got $1,800 left in the bank, $2,880 worth of unsold inventory sitting in your garage, and rent is due.

You’re stuck.

Planned inventory budgeting looks completely different.

Month one is about testing demand, not scaling production.

Instead of $3,200 on inventory, you spend $400 on materials to make 25 candles. You spend $150 on Shopify and a domain. You spend $300 on Instagram ads to test the market. You spend $50 on packaging materials.

Total month one investment is $900.

You sell 12 candles at $24 each, which is $288 revenue. You’re at a loss, but you’ve learned critical data. Your conversion rate is 2.1%—that’s 300 ad clicks with 12 purchases. Your best-selling scent is lavender vanilla, which was 7 of those 12 sales. Your customer acquisition cost is $25, which is $300 in ad spend divided by 12 customers.

That data is worth more than profit right now.

Month two is doubling down on what works.

You know lavender vanilla sells. You spend $600 on materials to make 75 candles, and 50 of them are lavender vanilla. You spend $150 on Shopify. You spend $500 on Instagram ads, but now you’re targeting people who engaged with your content in month one.

Revenue is $672 from 28 candles sold, and 22 of them were lavender vanilla.

You’re still at a loss—$1,250 spent, $672 earned—but your customer acquisition cost dropped to $17.85. Your conversion rate jumped to 3.8%.

You’re learning what works.

Month three is reaching break-even.

Materials cost $800 to make 100 candles, with 80% being lavender vanilla. Shopify is still $150. Ads are now $700 because you’re doing retargeting plus lookalike audiences.

Revenue is $1,152 from 48 candles sold.

Total spent in three months: $900 plus $1,250 plus $1,650 equals $3,800. Total earned: $288 plus $672 plus $1,152 equals $2,112. Net loss: negative $1,688.

But here’s what you have now. A proven product—lavender vanilla converts at 6.2%. A customer list of 88 buyers. A repeat purchase rate of 12.5% because 11 customers bought twice.

Month four is when you scale with confidence.

You know your numbers now:

- Average order value: $24

- Customer acquisition cost: $15 (optimized)

- Repeat purchase rate: 12.5%

- Lifetime value: $24 times 1.125 (accounting for repeat buyers) equals $27

Profit per customer is $27 minus $15 equals $12.

You can now budget for growth. If you spend $1,500 on ads, you’ll acquire 100 customers, make $2,700 revenue, and profit $1,200.

Months four through six budget plan:

- Ads: $1,500 monthly

- Inventory: $1,200 monthly (scales with projected sales)

- Shopify and tools: $200 monthly

Expenses are $2,900 monthly. Revenue is $4,050 monthly from 150 candles at $27 lifetime value. Profit is $1,150 monthly.

By month six, your bank balance is $5,000 starting money, minus $1,688 from the first three months loss, plus $3,450 from months four through six profit. That’s $6,762.

You’ve got 450 customers on your email list. You’ve got clear data on which products work.

Month seven brings a wholesale decision that most people get wrong.

A local boutique approaches you about selling your candles. They want 50 candles monthly at $12 each, which is 50% of your retail price.

The budget question is: is wholesale actually profitable?

Your current model per candle breaks down like this. Material cost is $8. Marketing cost is $7.50, which is your customer acquisition cost divided by average candles per order. Profit is $24 minus $8 minus $7.50 equals $8.50.

The wholesale model per candle looks different. Material cost is still $8. Marketing cost is $0 because the boutique handles that. Wholesale price is $12. Profit is $12 minus $8 equals $4.

Wholesale gives you $4 per candle versus $8.50 selling direct. But you don’t pay for ads.

The real question is: can you produce 50 extra candles without increasing fixed costs?

Your current production is 150 candles monthly. You make them yourself, spending 3 to 4 hours daily. Maximum capacity before hiring help is 200 candles monthly.

The plan: accept the wholesale order but cap it at 50 candles. This adds $200 monthly profit without increasing labor costs.

New month seven budget shows direct sales of 150 candles equaling $1,275 profit. Wholesale of 50 candles adds $200 profit. Total profit is $1,475 monthly.

Months eight through twelve are about hiring a part-time production assistant.

By month eight, you’re maxed out. You can’t make more than 200 candles monthly alone. To grow, you need help.

The hiring budget calculation looks like this. A part-time assistant working 20 hours weekly at $15 hourly costs $1,200 monthly. Additional workspace supplies add $100 monthly.

New fixed costs are $1,300 monthly.

To justify this hire, you need to produce enough extra candles to cover $1,300 plus maintain current profit.

The break-even calculation: at $8.50 profit per direct-sale candle, you need to sell an additional 153 candles monthly to cover the assistant’s cost. That’s $1,300 divided by $8.50.

With an assistant, you can produce 350 candles monthly—your 200 plus the assistant’s 150.

Month eight plan shows direct sales of 280 candles equaling $2,380 profit. Wholesale of 70 candles (you negotiated an increase) adds $280 profit. Total revenue profit is $2,660. Minus assistant cost of $1,300 equals net profit of $1,360.

You’re making less profit than month seven—$1,360 versus $1,475—but you’re working fewer hours. This is the trade-off planning forces you to see. Sometimes less profit with more freedom is the better choice.

By month twelve, you’ve scaled to 320 direct sales monthly and 100 wholesale candles monthly. You’ve got two part-time assistants. Monthly profit is $2,100.

Year-end bank balance: $23,432.

If You’re Building a SaaS Product

Software businesses are brutal because you spend for months before earning a single dollar.

Let’s say you’re building a project management tool for construction companies. You’ve saved $30,000 and you’ve got a technical co-founder, so no developer costs. Here’s how you plan to not die before launch.

Months one through four are pre-launch with zero revenue.

Your only costs are cloud hosting on AWS at $50 monthly, design tools like Figma at $15 monthly, domain and email at $15 monthly, and user testing incentives at $200 monthly.

Monthly burn is $280.

Most SaaS founders would add marketing here. They’d hire a salesperson. They’d get an office. You don’t. Your plan is simple: spend nothing until the product actually works.

Month four checkpoint shows money spent of $280 times four equals $1,120. Bank balance is $30,000 minus $1,120 equals $28,880. Runway remaining is 103 months at current burn rate.

Months five through six are private beta with your first revenue test.

You launch to 20 construction companies who agreed to test it. Your offer is straightforward: “Use it free for 60 days. If you find it valuable, $99 monthly after that.”

New costs include a customer support tool like Intercom at $74 monthly. Cloud hosting increases to $180 monthly because of more users. Email marketing through Mailchimp adds $20 monthly.

Monthly burn is now $554.

By month six, eight companies converted to paid. Revenue is $792 monthly.

Month six financials show revenue of $792 and burn of $554. Profit is $238.

You’re profitable on paper, but here’s the planning mistake many make. You’ve only got eight customers. If three churn, you’re at a loss again.

The SaaS planning rule is this: you need three to six months of revenue in the bank AFTER you’re cash-flow positive.

Your current monthly profit of $238 isn’t safety. You need $238 times six equals $1,428 saved as buffer before spending on growth.

Months seven through ten are buffer building.

You focus on retention and slow growth. No ads, no sales team. Just word-of-mouth and referrals.

Month seven brings 11 customers, $1,089 revenue, $554 expenses, $535 profit.

Month eight brings 14 customers, $1,386 revenue, $554 expenses, $832 profit.

Month nine brings 17 customers, $1,683 revenue, $620 expenses, $1,063 profit.

Month ten brings 21 customers, $2,079 revenue, $680 expenses, $1,399 profit.

Buffer at month ten is $535 plus $832 plus $1,063 plus $1,399 equals $3,829.

You’ve built a 5.6-month runway. That’s $3,829 divided by $680 current burn. Now you can invest in growth.

Month eleven is your first growth investment.

You hire a part-time salesperson on commission only, 20% of new sales. You start cold email outreach using a tool that costs $99 monthly.

New burn is $779 monthly for base costs plus tools.

You close eight new customers in month eleven. Revenue jumps to $2,871. But you pay $158 in commissions—that’s eight customers times $99 times 20%.

Month eleven profit is $2,871 minus $779 minus $158 equals $1,934.

Month twelve is the scaling checkpoint.

You’ve got 35 customers now. Revenue is $3,465. Costs are $779 base plus $316 commissions equals $1,095 total. Profit is $2,370.

Year-end bank balance starts at $28,880 after month four. Add month six profit of $238. Add months seven through ten buffer of $3,829. Add month eleven profit of $1,934. Add month twelve profit of $2,370.

Total: $37,251.

You have more money than when you started, despite building a product from scratch. That’s what disciplined budget planning does.

If You’re Opening a Restaurant

Restaurants have the worst cash flow of any business. You pay for food daily, rent monthly, and staff weekly. But customers pay per meal.

Let’s say you’re opening a fast-casual restaurant with $80,000 saved. Here’s how you plan not to become another failure statistic, because 60% of restaurants fail in year one.

The standard restaurant mistake is spending $60,000 on buildout and equipment, $15,000 on inventory, $5,000 on marketing. You open with $0 buffer. You run out of money by month three when revenue doesn’t meet projections.

The planned approach uses the 50-30-20 rule.

50% goes to buildout and equipment, which is $40,000. 30% is kept as operating buffer, which is $24,000. 20% goes to opening inventory and marketing, which is $16,000.

Your buildout is bare-bones. You buy used equipment. You do a minimal renovation. You focus on speed to opening—45 days instead of the usual four months.

Month one is a soft opening, not a grand opening.

You don’t do a grand opening. You do a soft opening with limited hours—11am to 3pm, five days weekly.

Why? To test operations without full costs.

Month one costs break down like this:

- Rent: $3,500

- Utilities: $600

- Part-time staff, two people at 20 hours weekly each: $1,400

- Food costs with a limited menu: $1,800

- Supplies and miscellaneous: $300

Total is $7,600.

Revenue for the first month with limited hours is $4,200.

Loss is negative $3,400.

But you learned critical things. Most popular dish is chicken shawarma bowl at 38% of orders. Peak hours are 11:30am to 1pm, which is 67% of sales. Waste percentage is 12%, and industry average is 4% to 10%, so you’re high.

Month two is fixing waste and extending hours.

You cut the menu from 12 items to seven, eliminating low sellers. You extend hours to 11am to 8pm, six days weekly.

New costs:

- Rent: $3,500

- Utilities: $800

- Staff, three people now at 30 hours weekly: $3,150

- Food costs: $4,200

- Supplies: $450

Total is $12,100.

Revenue is $11,800.

Loss is negative $300.

You’re nearly break-even. Your waste dropped to 6%. Your chicken shawarma bowl now represents 52% of sales, so you negotiated bulk pricing on chicken. You’re saving $280 monthly.

Month three is reaching profitability.

Same hours, same staff. You’re focused on speed and consistency.

Revenue is $15,400. Costs are $11,820. Profit is $3,580.

Month three checkpoint shows total spent over three months of $40,000 for buildout, $16,000 for opening costs, $7,600 month one, $12,100 month two, $11,820 month three. That’s $87,520 total.

Total earned is $4,200 plus $11,800 plus $15,400 equals $31,400.

Bank balance is $80,000 minus $87,520 plus $31,400 equals $23,880.

You burned through $56,120 in three months, but you’re profitable now. Most restaurants would’ve spent the full $80,000 on buildout and been bankrupt by now.

Months four through six are building cash reserves.

You stay disciplined. No expansion, no new equipment. Just consistent operations.

Month four shows $16,800 revenue, $12,100 costs, $4,700 profit.

Month five shows $18,200 revenue, $12,400 costs, $5,800 profit.

Month six shows $19,500 revenue, $12,800 costs, $6,700 profit.

Bank balance at month six is $23,880 plus $4,700 plus $5,800 plus $6,700 equals $41,080.

Now you’ve got a decision. Do you expand hours and open for breakfast, or do you open a second location?

The budget planning answer is clear. To add breakfast service, you need to hire two more staff members for morning shifts. That’s $2,400 monthly added to costs. You need to buy breakfast-specific equipment like a griddle and waffle maker. That’s $3,500 upfront. You need to increase food costs by about $1,800 monthly for breakfast ingredients.

New monthly costs would be $12,800 plus $2,400 plus $1,800 equals $17,000.

To break even, you need breakfast to generate $4,200 in additional revenue monthly. That’s 140 breakfast customers at an average check of $30.

Can you realistically get 140 breakfast customers in a month when you’re new? That’s 7 customers per breakfast service if you’re open 20 days monthly.

Probably not in month seven.

So you delay breakfast. Instead, you focus on optimizing dinner service, which already works. You extend dinner hours to 9pm instead of 8pm. That costs nothing extra in labor because your existing staff just works one more hour. You add a happy hour menu from 3pm to 5pm to fill the dead zone between lunch and dinner.

Month seven shows $22,100 revenue from extended dinner hours and happy hour. Costs stay at $13,200. Profit is $8,900.

By month nine, you’re consistently hitting $24,000 monthly revenue with $13,500 costs. Profit is $10,500 monthly.

Bank balance at month nine is $41,080 plus $8,900 plus $9,800 plus $10,500 equals $70,280.

Now breakfast makes sense. You’ve got the cash buffer to absorb three months of breakfast losses while you build the customer base.

Month ten launches breakfast service.

You hire two breakfast staff. You buy the equipment. You start promoting breakfast on social media two weeks before launch.

Month ten shows breakfast revenue of $2,800 from 93 customers. Total revenue including lunch and dinner is $26,800. Total costs jumped to $17,300 because of new staff and food costs.

Profit is $9,500.

Breakfast didn’t break even, but you knew it wouldn’t in month one. You planned for a three-month ramp.

Month eleven shows breakfast revenue of $4,100. Total revenue is $28,300. Costs are $17,400. Profit is $10,900.

Month twelve shows breakfast revenue of $5,200. Total revenue is $29,700. Costs are $17,600. Profit is $12,100.

Year-end bank balance is $70,280 plus $9,500 plus $10,900 plus $12,100 equals $102,780.

You’ve got enough cash now to consider a second location, but the smart plan is waiting until year two. You want 18 months of operations data before replicating the model.

The Real Difference Between Planning and Guessing

Most people confuse budgeting with planning. Budgeting is saying “I’ll spend $5,000 on marketing.” Planning is saying “I’ll spend $300 in month one to test conversion rates, then $800 in month two if conversion is above 2%, then $1,500 in month three if customer acquisition cost is below $25.”

See the difference?

Planning has conditional logic. If this happens, then I do that. If this metric hits this threshold, then I invest more. If this metric drops below this number, then I cut costs here.

When you’re starting a business, you don’t know what will work. So your budget plan should reflect that uncertainty.

Here’s a framework that works across every business type:

Phase One: Validation (Months 1-3)

Spend the minimum to test your core hypothesis. For agencies, that’s “can I close clients with this offer?” For e-commerce, it’s “will people buy this product?” For SaaS, it’s “will users pay for this solution?” For restaurants, it’s “will people eat this food at this price?”

Your budget should be tiny. Just enough to get real market feedback.

Phase Two: Optimization (Months 4-6)

You’ve validated that something works. Now you’re improving the unit economics. Lower customer acquisition cost. Increase conversion rates. Reduce waste. Improve margins.

Your budget increases, but you’re laser-focused on efficiency metrics.

Phase Three: Scaling (Months 7-9)

You’ve got proven unit economics. Now you pour fuel on the fire. Increase ad spend. Hire people. Extend hours. Add locations.

Your budget expands significantly, but it’s backed by data.

Phase Four: Systematizing (Months 10-12)

You’re building systems so growth doesn’t break operations. Hire managers. Implement software. Create processes. Document everything.

Your budget shifts from growth to infrastructure.

Each phase has different goals, different spending priorities, different success metrics.

The Cash Flow Safety Formula

Here’s the formula that’s saved more businesses than any other piece of advice:

Your runway equals your bank balance divided by your monthly burn rate.

Runway should never drop below six months. Ever.

If your bank balance is $20,000 and your monthly burn is $4,000, your runway is five months. You’re in danger. You need to either increase revenue immediately or cut costs immediately.

Most business failures happen because founders don’t track runway weekly. They check their bank balance once a month and think they’re fine. Then they wake up one day with two months of runway and realize they can’t turn things around fast enough.

Track runway weekly. Every Monday morning, calculate it. Bank balance divided by monthly burn. If it’s below six months, sound the alarm.

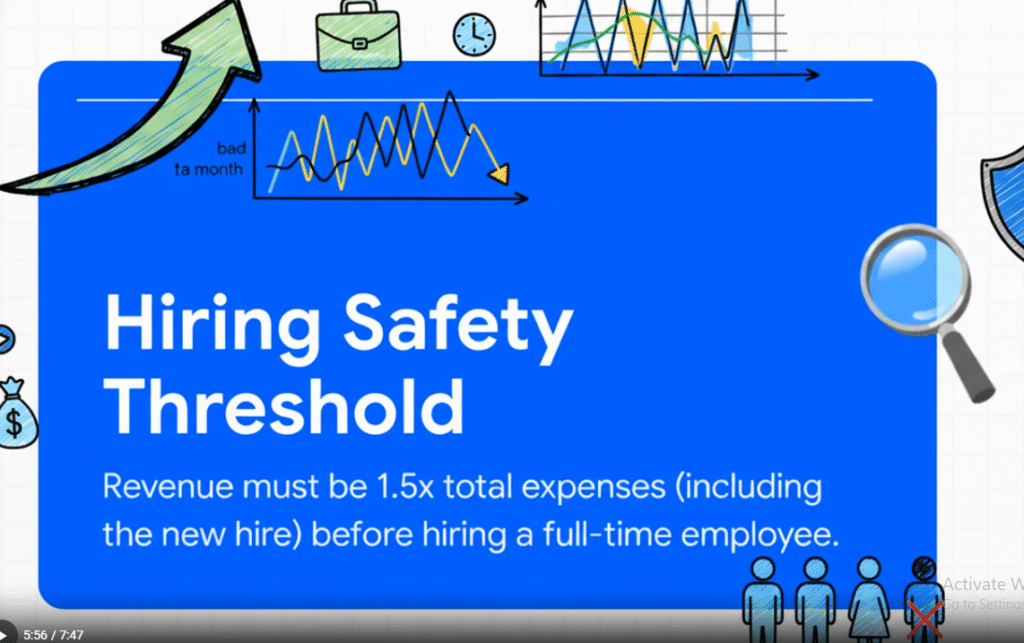

The Hiring Safety Threshold

Never hire full-time employees until your revenue is 1.5 times your total expenses including the new hire.

Let’s say you’re making $15,000 monthly revenue with $5,000 in expenses. You want to hire someone at $4,000 monthly (including taxes and benefits).

Your new total expenses would be $9,000. Your revenue needs to be $13,500 to meet the 1.5x threshold. You’re at $15,000, so you’re safe.

But if your revenue was $12,000, you’d be at 1.33x. Too close. One bad month and you can’t make payroll.

The 1.5x rule gives you breathing room for revenue fluctuations, client churn, seasonal dips, or unexpected expenses.

The Inventory Planning Rule for Physical Products

Never buy more than 30 days of inventory until you’ve sold through three complete inventory cycles.

If you’re selling candles and your first batch is 50 candles, don’t order 500 candles until you’ve sold through 50 candles three separate times. Why? Because you need to learn your sell-through rate, your return rate, your damage rate, and your seasonal fluctuations.

Inventory is cash sitting on a shelf. Every dollar in inventory is a dollar you can’t use for marketing, can’t use for hiring, can’t use for growth.

Start small. Sell through. Reorder. Repeat. Only scale inventory purchasing after you’ve got solid data.

The Service Business Payment Terms Strategy

If you’re running a service business, payment terms will make or break you.

Option one: NET-30 payment terms. Clients pay 30 days after invoice. This is standard, but it destroys your cash flow in the first six months.

Option two: 50% upfront, 50% on delivery. This is better. You get half the money before doing the work, which funds your expenses.

Option three: Monthly retainer paid at the beginning of the month. This is best. Clients pay on the first of the month for that month’s work. Your revenue is predictable and your cash flow is immediate.

Start with option two until you have enough clients to offer option three. Never start with option one unless the client is huge and you’ve got six months of runway in the bank.

The Pricing Test Framework

Most businesses underprice in year one because they’re scared of losing customers. But underpricing is more dangerous than overpricing.

Here’s how to test pricing without killing your business:

Month one through three: Price at market rate (check what competitors charge).

Month four: Raise prices 20% for all new clients. Keep existing clients at the old rate.

Track close rate. If your close rate drops below 30%, your price is too high. If your close rate stays above 50%, your price is too low.

Month five: Adjust based on data. If close rate was 45%, raise another 10%. If it was 25%, drop 15%.

Month six: Lock in your price based on data, not feelings.

Most businesses discover they can charge 30% to 50% more than they initially thought. That extra margin is your safety buffer when things go wrong.

The Emergency Fund Rule

Beyond your six-month runway, you need an emergency fund equal to three months of expenses.

This is separate from operating capital. This is “the roof just caved in” money or “my biggest client just left” money or “I need emergency dental surgery” money.

If your monthly expenses are $8,000, you need $24,000 in an emergency fund that you never touch unless it’s an actual emergency.

Most business owners skip this. Then an emergency hits and they have to put it on a credit card at 22% interest. Now they’re not just dealing with the emergency—they’re dealing with debt payments that reduce their monthly cash flow forever.

Build the emergency fund in months seven through twelve after you’re profitable. Set aside 20% of profit each month until you hit three months of expenses.

The Expansion Timing Formula

When should you open a second location, launch a second product, or enter a second market?

The formula: when you’ve achieved 12 consecutive months of profitability AND you have data showing demand in the new area.

Not 12 months of revenue. 12 months of profit.

And not just gut feeling about demand. Actual data. Surveys, waitlists, pre-orders, or beta testers.

Most businesses expand too early because they confuse revenue growth with business health. You can be growing revenue and still be unprofitable. Expansion before profitability is how you go from struggling in one location to bankrupt in two.

Wait until the core business is systematized and profitable. Then expand with data, not hope.

What Actually Matters in Year One

Budget planning isn’t about perfect forecasts. You’ll be wrong about half your assumptions.

It’s about building in safety margins so being wrong doesn’t kill you.

It’s about tracking the right metrics weekly so you see problems coming three months before they arrive.

It’s about having conditional plans—if revenue drops below X, I cut cost Y. If customer acquisition cost rises above Z, I pause ads and focus on organic.

The businesses that survive year one aren’t the ones with the best products. They’re the ones who planned for the worst-case scenario and built buffers into everything.

Track your runway weekly. Keep it above six months. Use the 1.5x rule before hiring. Test pricing aggressively. Build an emergency fund. Don’t expand until you’ve got 12 months of profit.

That’s how you avoid financial stress. Not by hoping things go well, but by planning for when they don’t.

Check some others related post:

- When discussing growth strategies or entrepreneurship, link to Business for deeper insights into industry trends and case studies.

- In articles about digital transformation or emerging tools, connect to Technology to guide readers toward tech innovations.

- While covering branding, campaigns, or customer engagement, embed Marketing to provide actionable marketing strategies.

- For topics on investments, budgeting, or global markets, link to Finance to strengthen financial context.

- When writing about workflow optimization or automation tools, reference AI Business Automation to highlight practical AI-driven solutions.

- In discussions of machine learning, neural networks, or AI ethics, embed Artificial Intelligence for readers seeking technical depth.

Some people also ask:

You need enough to cover 4-6 months of expenses before your first payment arrives. For service businesses, this means calculating your monthly burn rate (around $2,600-$4,200 for a basic agency) times four, since clients typically pay on NET-30 terms. If you’re launching with $12,000, you can afford about $3,000 monthly in costs. The critical mistake is planning for revenue instead of planning for cash flow—you’ll spend money weekly but receive payments monthly, creating a dangerous gap that kills most businesses by month three.

Hire full-time only when your revenue is 1.5 times your total expenses including the new hire’s cost. For example, if you’re making $18,900 monthly with $4,200 in expenses and want to hire someone at $4,105 monthly (salary plus taxes and benefits), your new total expenses would be $8,305. You need revenue of at least $12,458 to meet the safety threshold. The 1.5x rule protects you from revenue fluctuations—if you hire at exactly 1:1 ratio and lose one major client, you can’t make payroll. Always grow to 20+ clients before transitioning from freelancers to employees.

Never buy more than 30 days of inventory until you’ve sold through three complete cycles. Start with $400-$600 in materials to make 25-50 units, not $3,200 for 200 units. In month one, you’re testing which products actually sell and what your conversion rate is. After three sell-through cycles, you’ll know your waste percentage (should be 4-10%), your best-sellers (typically one product drives 50%+ of sales), and your actual customer acquisition cost. Only then should you negotiate bulk pricing and scale inventory. Every dollar in unsold inventory is cash you can’t use for marketing or operations.

Budgeting is saying “I’ll spend $5,000 on marketing.” Planning is saying “I’ll spend $300 in month one to test conversion rates, then $800 in month two if conversion is above 2%, then $1,500 in month three if customer acquisition cost is below $25.” Planning has conditional logic with specific thresholds. It answers: if this metric hits this number, then I do this action. Real planning tracks runway weekly (bank balance divided by monthly burn), requires six months minimum runway at all times, and has if-then scenarios for when revenue drops or costs spike. Budget planning prevents crisis; budgeting just records it.

You’re safe to scale when you hit three conditions simultaneously: 12 consecutive months of profit (not just revenue), runway above six months, and proven unit economics. For agencies, this means customer acquisition cost under $25 and lifetime value above $1,200. For e-commerce, it means conversion rates above 3% and repeat purchase rates above 12%. For SaaS, it means monthly churn below 5% and at least 35 paying customers. The specific numbers vary by industry, but the principle is identical—you need sustained profitability, cash reserves, and data proving your model works before spending money on expansion, new locations, or additional products.