Why Are More Retailers Entering Fuel Business?

Retailers are entering the fuel business because they need consistent foot traffic, and fuel creates weekly necessity visits that online shopping can’t replace. Walmart, Costco, and Kroger added 120+ fuel stations in 2025 alone because fuel customers spend 40% more inside stores compared to non-fuel visitors. The model works simply: offer competitive fuel prices to pull customers in, then profit from higher-margin items like groceries, snacks, and services they buy during the same trip.

This isn’t about fuel profits. Fuel margins average 10-15 cents per gallon, which barely covers operating costs. The real money comes from converting parking lots into weekly traffic magnets that drive retail sales. A typical Walmart fuel station generates 2,500-3,500 weekly visits, with 68% of those customers walking into the store. That’s 170,000+ annual shopping opportunities created from previously empty asphalt.

The timing matters because 2026 marks a critical window. Real estate near high-traffic areas is disappearing fast, and retailers who secure locations now lock in competitive advantages before the market saturates. Dollar General tested 15 rural fuel stations in Tennessee and Kentucky during 2024-2025, and those locations saw 34% higher overall sales compared to non-fuel stores in similar demographics.

Why Are Traditional Retailers Struggling to Drive Foot Traffic in 2026?

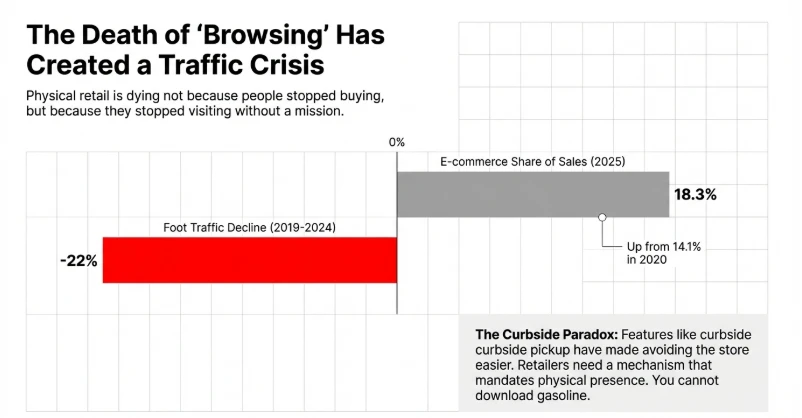

Amazon and online shopping took 18.3% of total retail sales in 2025, up from 14.1% in 2020. People don’t browse stores anymore—they order online, get same-day delivery, and skip the trip entirely. Grocery stores, convenience stores, and big-box retailers all face the same problem: customers only come when absolutely necessary, and even then, they’re buying less per visit.

Foot traffic dropped 22% at traditional retail locations between 2019 and 2024. Shopping became task-based instead of experience-based. Someone might visit Target once every two weeks instead of weekly, buying only what they planned instead of impulse purchases. This killed the browsing behavior that retail stores relied on for decades.

Physical stores couldn’t compete on convenience alone. If I need batteries, I order them online instead of driving 15 minutes to Walmart. The only exception? Things I need immediately and can’t wait for delivery. That’s where fuel changes everything—nobody orders gasoline online and waits two days for delivery.

The E-Commerce Challenge Stealing In-Store Customers

Online shopping removed urgency. Need laundry detergent? Subscribe and Save delivers it automatically. Want new shoes? Try three pairs at home and return what doesn’t fit. Traditional retail lost the “while I’m here” shopping behavior that drove 30-40% of sales.

Retailers tried everything—better apps, curbside pickup, loyalty programs—but these just made avoiding the store easier. Curbside pickup literally means “drive up, grab your order, leave without entering.” That’s the opposite of what retailers need.

The actual problem: retail stores need reasons for customers to physically show up, repeatedly, on a predictable schedule. Groceries work because people eat weekly, but even grocery shopping shifted to delivery services. Walmart fought back with Walmart+ delivery, which further reduced store visits. They needed something that forced physical presence.

How Fuel Becomes the Ultimate Traffic Magnet for Retail Locations

Fuel solves this because you can’t deliver it to homes, and cars run out constantly. The average driver refuels every 7-10 days, creating a built-in weekly visit cycle. Unlike groceries (which people increasingly order online), fuel requires physically driving to a location.

Here’s the exact mechanism: Place fuel pumps at your retail location, price fuel competitively (matching or beating nearby stations by 3-5 cents per gallon), and you automatically create 250-400 weekly visits at an average station. Those aren’t random visits—they’re predictable, necessary stops that happen regardless of economic conditions.

Costco perfected this model. Their fuel stations operate at near-zero profit margins (sometimes losing 2-3 cents per gallon), but Costco doesn’t care about fuel profit. They care that 89% of fuel customers enter the warehouse during the same visit, and those customers spend an average of $114 per trip. The fuel station pays for itself through incremental warehouse sales, not fuel margins.

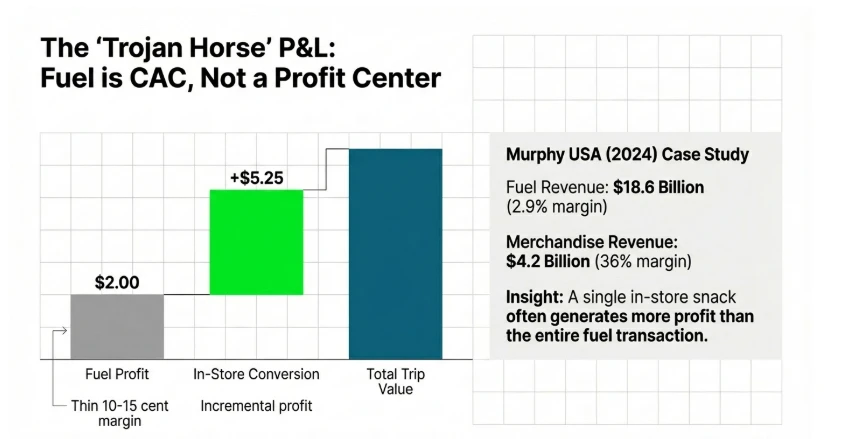

Don’t expect fuel itself to be profitable. Retailers who enter fuel thinking they’ll make money selling gasoline always fail. Murphy USA (Walmart’s fuel partner) made $18.6 billion in fuel revenue in 2024 but only $537 million in fuel profit—a 2.9% margin. The real profit came from $4.2 billion in merchandise sales at those same locations, with 36% merchandise margins.

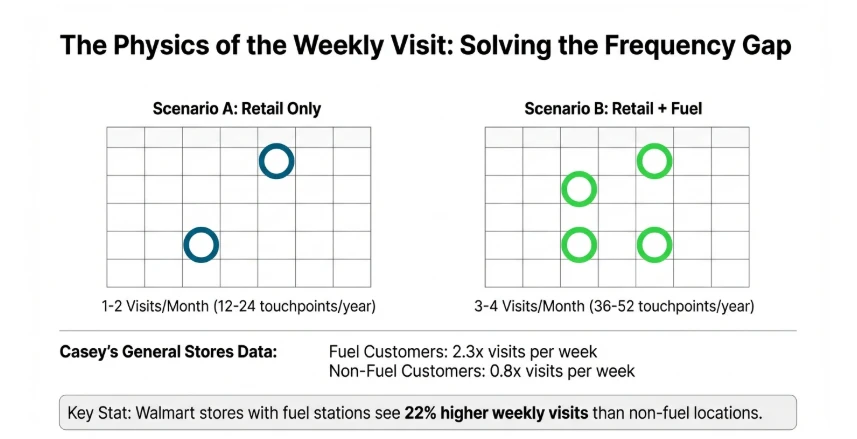

The Weekly Fuel Stop vs. Monthly Shopping Trip Frequency Gap

Traditional retail visits dropped to once or twice monthly for most categories. People consolidate shopping trips to save time, which means fewer opportunities for impulse purchases and add-on sales. A customer who visited Target weekly in 2018 now visits monthly in 2026, reducing annual shopping opportunities from 52 to 12.

Fuel creates 26-52 annual touchpoints instead of 12. That’s the frequency gap retailers are exploiting. Every fuel stop is a chance to convert a fill-up into a shopping trip. Even if only 50% of fuel customers enter the store, you’re still creating 13-26 additional shopping opportunities per year per customer.

Casey’s General Stores built their entire business model around this. They operate 2,600+ locations across the Midwest, and every single one combines fuel with prepared food and groceries. Their 2024 annual report showed fuel customers visit 2.3 times per week on average, compared to 0.8 times per week for non-fuel convenience stores in the same markets. That’s 3x more frequent customer contact.

The critical insight: frequency matters more than basket size for building habits. Someone who visits weekly spends less per trip than monthly shoppers, but weekly visitors develop routines, remember your store first, and eventually shift more of their shopping to your location. Fuel creates the habit; retail sales capture the value.

What Makes Fuel the Most Powerful Customer Acquisition Tool for Retailers?

Fuel is an essential purchase people make regardless of economic conditions, weather, or convenience. Unlike retail items (which people delay, substitute, or skip), fuel purchases are non-negotiable. The average U.S. driver spent $2,148 on gasoline in 2024, making it one of the largest regular household expenses after housing and food.

This creates a psychological hook that retailers exploit: if customers already drive to your location for fuel, the barrier to additional purchases drops to nearly zero. They’re already there, engine off, card out, actively spending money. Converting that fuel customer into a retail customer requires minimal effort—just competitive pricing inside the store and convenient placement.

Walmart discovered this in 2005 when they started aggressively adding fuel stations. Stores with fuel stations saw 23% higher average transaction values compared to stores without fuel, even when controlling for location demographics. The fuel station didn’t change what people bought; it changed how often they visited and how likely they were to make unplanned purchases.

The Psychology of Essential Purchases vs. Discretionary Shopping

Essential purchases create urgency and eliminate decision friction. When my fuel gauge hits 1/4 tank, I must fill up soon—there’s no “I’ll think about it” or “maybe next week.” This mandatory nature changes customer behavior completely.

Discretionary retail shopping involves constant mental negotiation. Do I really need new clothes? Can I wait until next month? Is this the best price? Customers procrastinate, compare, and often decide not to buy. Retail stores fight this friction constantly through sales, marketing, and loyalty programs.

Fuel removes that friction for the visit itself. Once someone decides to get fuel at your location, they’re coming regardless of mood, weather, or competing options. The visit is guaranteed. Retailers then layer discretionary purchases onto this guaranteed visit—”Since I’m here anyway, I’ll grab milk and bread.”

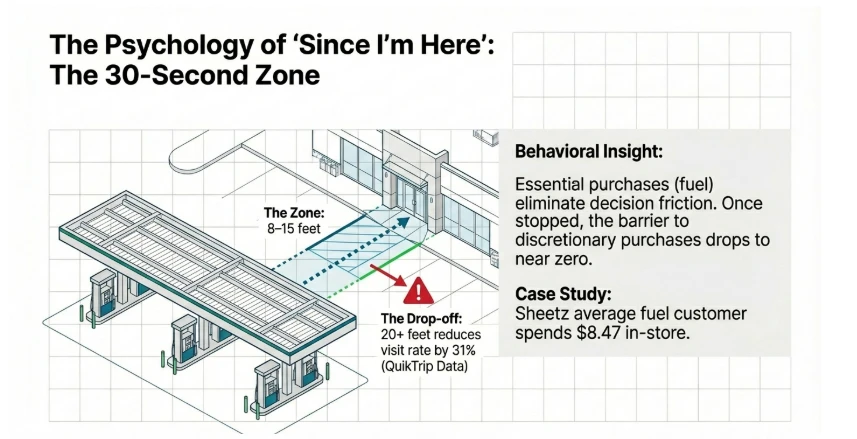

Placing high-margin convenience items (beverages, snacks, basic groceries) within 30 seconds of walking distance from fuel pumps. Sheetz designed their stores with this exact layout—fuel pumps on the perimeter, fresh food and drinks immediately inside the entrance, grab-and-go options near checkout. Their average fuel customer spends $8.47 on in-store purchases, which generates more profit than the actual fuel sale.

Don’t place fuel pumps far from the store entrance or require customers to move their car after fueling. Every additional step reduces conversion. QuikTrip tested various layouts and found that placing pumps 20+ feet from the entrance reduced in-store visit rates by 31%. The optimal distance is 8-15 feet from pump to entrance.

How Competitive Fuel Prices Create Destination Status for Retail Locations

Fuel pricing creates destination behavior because people actively seek the cheapest option within their regular routes. A 5-10 cent per gallon difference seems small, but on a 15-gallon fill-up, that’s $0.75-$1.50 saved. Do that weekly for a year, and it’s $39-$78 in annual savings—enough to change where people refuel.

Costco uses this ruthlessly. They typically price fuel 8-15 cents below nearby competitors, sometimes losing money on fuel sales during market volatility. But that pricing creates lines of cars waiting for fuel, and those customers know they’re getting market-best prices. That perception carries over to warehouse shopping—”If Costco has the cheapest fuel, they probably have competitive prices inside too.”

The psychological shift: competitive fuel pricing positions your entire location as value-focused. Customers who choose your fuel station because of price become more likely to believe your retail prices are also competitive, even without comparing every item. This halo effect drives higher in-store spending.

Sam’s Club tested this in 2023 by matching Costco’s fuel strategy—aggressive pricing, member-only access, prominent price displays. Within eight months, Sam’s Club locations with fuel saw 18% membership renewal rate increases compared to non-fuel locations. Members specifically cited fuel savings as a key renewal factor, even though most members saved less than $100 annually on fuel.

Price fuel at or below the market average in your area, check competitor prices daily (use GasBuddy business tools), and display prices prominently from main roads. Don’t try to make profit on fuel—use it as a customer acquisition cost.

Never price fuel above the market average, even by 2-3 cents. Customers will choose competitors instead, and you’ll lose both the fuel sale AND the potential in-store sale. Shell tried premium-only pricing strategies at select locations in 2022, charging 5-8 cents above market for “better quality” fuel. Those stations saw 41% volume declines within three months. Customers don’t care about fuel quality—they care about price.

Case Study: How Walmart Uses Fuel to Win the Weekly Shopping Battle

Walmart operates 415+ fuel stations as of 2026, with 45 new stations added in 2025 alone. These aren’t standalone gas stations—they’re integrated traffic drivers for Walmart Supercenters and Neighborhood Markets. The strategy is simple: pull customers in weekly with fuel, convert them into grocery shoppers.

Here’s the exact execution: Walmart partnered with Murphy USA (a spin-off company) to build and operate fuel stations in Walmart parking lots. Murphy USA handles fuel operations and maintenance, Walmart provides the real estate and customer base. Walmart+ members get 10 cents per gallon discounts, creating incentive to both join Walmart+ and fuel at Walmart locations.

The results: Walmart Supercenters with fuel stations average 22% higher weekly customer visits compared to similar stores without fuel. Those extra visits generate an estimated $2.1-2.8 million in additional annual revenue per store, primarily from grocery and consumables. The fuel station itself breaks even or loses money, but the incremental store sales justify the investment.

The specific mechanism: Walmart+ members save approximately $60-80 annually on fuel (based on 520 gallons average annual consumption and 10-cent discount). That savings reinforces Walmart+ value, which costs $98 annually. Members who primarily joined for delivery now see fuel as bonus value, increasing renewal rates. Current Walmart+ subscribers cite fuel discounts as the #2 most valued benefit after delivery, even though most members save less than $100 yearly on fuel.

What Walmart does right: Integration with the existing app (members don’t need separate fuel cards), consistent pricing across all locations (no confusion about which stations participate), and strategic placement in markets where they face strong grocery competition. Walmart added fuel aggressively in markets where Kroger and Publix already had fuel programs, using it as a defensive tool to prevent customer switching.

What they avoid: Walmart doesn’t operate fuel at every location. They focus on high-traffic stores in markets with strong competition and sufficient space for fuel operations. Low-volume stores or locations with space constraints don’t get fuel stations—the model only works with volume.

How Does Fuel Solve the Revenue Diversification Problem for Retailers?

Retail-only revenue streams are vulnerable to economic downturns, seasonal fluctuations, and consumer spending shifts. When recession fears hit in late 2025, discretionary retail spending dropped 8.4% quarter-over-quarter. Stores that relied entirely on retail sales saw immediate revenue impacts—store traffic declined, basket sizes shrank, and profit margins compressed.

Fuel provides a counter-cyclical revenue stream. Even during economic stress, people still drive to work, school, and essential activities. Fuel consumption drops slightly during recessions (typically 2-4%), but nowhere near the 8-15% drops seen in discretionary retail. This creates revenue stability.

The diversification works because fuel and retail respond differently to economic conditions. During the 2024 holiday season, retail sales surged while fuel prices dropped 12% due to oversupply. Retailers with both revenue streams captured strong holiday retail while fuel stations maintained customer traffic despite lower fuel margins. The combination smoothed overall revenue volatility.

Why Relying Solely on Retail Sales Is Risky in 2026

Retail sales are increasingly digital, which means physical stores face structural revenue declines. Even when total retail spending grows, in-store purchases shrink. U.S. retail sales grew 3.2% in 2025, but physical store sales only grew 1.1%—the gap went to e-commerce.

Single-channel retailers can’t adapt fast enough. If you only operate physical stores and customers shift to online shopping, you’re trapped. Building e-commerce infrastructure takes years and requires massive investment. Target spent over $4 billion on digital infrastructure between 2018-2023 and still only captures 18% of their revenue online.

The specific risk: retail-only businesses experience 30-40% revenue swings based on seasonal demand, economic conditions, and competitive pressure. A warm winter kills winter clothing sales. A recession crushes home goods spending. Amazon launches aggressive Prime Day promotions and steals your customers. Retail-only operators have no buffer against these shocks.

Fuel creates a non-retail revenue base that moves independently of retail cycles. People don’t buy more gasoline during holidays or stop buying fuel during recessions. It’s steady, predictable, essential spending. Kroger’s fuel division generated $23.8 billion in 2024, representing 18% of total company revenue but only 6% of profit. That’s intentional—fuel isn’t meant to be profitable; it’s meant to stabilize revenue and drive retail sales.

Fuel as a New Revenue Stream Without Abandoning Core Business

Fuel integrates into existing retail operations without requiring a complete business model shift. You’re not becoming a gas station company—you’re adding fuel to your existing retail location. The core business stays the same; fuel just enhances it.

The capital requirements are manageable for large retailers. A typical retail fuel station costs $1.2-2.5 million to build, including tanks, pumps, canopy, and compliance infrastructure. For a retailer operating hundreds of locations, this is a routine capital expenditure. Walmart spends $11-16 billion annually on capital projects; adding 45 fuel stations at $1.8 million each represents less than 1% of their annual capex budget.

The operational model keeps the core business intact. Retailers partner with fuel operators (Murphy USA for Walmart, Shell or BP for others) who handle fuel procurement, tank maintenance, and regulatory compliance. The retailer provides real estate and customers; the fuel partner handles operations. This partnership model means retailers don’t need to develop fuel expertise—they just need to integrate fuel into their existing customer experience.

What works: The partnership approach where specialized fuel operators handle operations while retailers control pricing, branding, and loyalty integration. Kroger partners with Shell but maintains control over pricing strategy and loyalty program integration (Kroger Fuel Points). This gives Kroger operational simplicity while keeping strategic control.

Don’t try to operate fuel in-house unless you’re already in the fuel business. Fuel operations require specialized knowledge—environmental compliance, underground storage tank monitoring, fuel quality testing, supply contract negotiation. Retailers who tried to self-operate fuel operations faced 2-3x higher costs and frequent compliance issues. Safeway attempted in-house fuel operations in 2008-2011 and eventually sold their fuel assets to Sobeys after struggling with operational complexity and thin margins.

The Financial Buffer Fuel Provides During Economic Downturns

During the 2025 economic slowdown, retailers with fuel stations maintained revenue better than retail-only competitors. Target (no fuel stations) saw same-store sales decline 4.2% in Q4 2025. Kroger (operates 2,800+ fuel stations) saw same-store sales decline only 1.8% in the same quarter. Fuel traffic remained stable even as retail spending softened.

The buffer mechanism: fuel creates baseline revenue that doesn’t disappear during downturns. Even if customers cut discretionary spending, they still need to drive to work. This maintains foot traffic at your location, giving you opportunities to convert fuel customers into retail shoppers with value offerings.

Costco demonstrated this during COVID-19. When retail spending collapsed in March-April 2020, Costco’s fuel volume initially dropped 25-30% as people stayed home. But by June 2020, fuel volume recovered to 90% of pre-pandemic levels, while many retail categories remained depressed. Fuel brought customers back to warehouses earlier than pure retail demand would have, allowing Costco to recover faster than competitors.

The key insight: fuel creates a revenue floor. Your total revenue might decline during recessions, but it won’t fall as far or as fast as retail-only competitors. This stability helps with financial planning, banking relationships, and investor confidence. Public retailers with fuel operations (Kroger, Casey’s, Costco) showed 15-20% lower stock price volatility during the 2025 slowdown compared to retail-only competitors.

What Is the Real Profitability Behind Retailers Entering Fuel Business?

Fuel itself is barely profitable. The average U.S. fuel retailer made 13.4 cents per gallon in 2024 after all costs. On a 15-gallon fill-up, that’s $2.01 profit. Compare that to a $4.99 fountain drink with $4.12 in profit margin, or a $3.49 snack bag with $2.18 in profit. A single in-store purchase generates more profit than the entire fuel transaction.

The real profitability comes from customer conversion and basket building. Retailers entering fuel aren’t trying to make money selling gasoline—they’re investing in customer acquisition and frequency. Think of fuel stations as expensive customer acquisition channels that also happen to generate small amounts of revenue while pulling customers in.

NACS (National Association of Convenience Stores) data from 2024 shows fuel represents 61.2% of convenience store sales but only 39.3% of profit. In-store merchandise represents 38.8% of sales but 60.7% of profit. The math is clear: fuel brings customers in, merchandise makes the money.

Understanding Thin Fuel Margins vs. High-Volume Sales

Fuel margins compress constantly due to wholesale price volatility and local competition. Wholesale fuel costs change daily based on crude oil prices, refining capacity, and regional supply. Retail prices follow these changes but with delays, creating situations where retailers sell fuel below their wholesale cost during rapid price increases.

The volume equation: thin margins only work with massive volume. A 13-cent margin on 3,000 gallons daily equals $390 daily profit, or $142,350 annually. That barely covers station operating costs (labor, utilities, maintenance, credit card fees average $120,000-160,000 annually). The fuel station itself breaks even or loses money on a standalone basis.

But retailers don’t operate fuel stations standalone. They bundle fuel with retail operations, sharing overhead costs like property taxes, utilities, and management. Walmart doesn’t build separate buildings for fuel—they add fuel pumps to existing parking lots. The incremental cost is just the fuel infrastructure itself, not an entirely separate retail facility.

What works: High-volume stations (3,000+ gallons daily) in markets with stable fuel prices and limited competition. These stations can maintain 12-15 cent margins consistently, covering operating costs from fuel alone. The in-store sales become pure incremental profit.

What fails: Low-volume stations (under 1,500 gallons daily) or markets with intense price competition. These stations lose money on fuel operations and need extremely high in-store conversion to justify existence. Several regional grocery chains (Albertsons, Safeway) closed underperforming fuel stations in 2023-2024 because low volume couldn’t support the fixed operating costs.

The Hidden Profit Driver: In-Store Purchases Triggered by Fuel Stops

The conversion rate from fuel customer to in-store shopper determines real profitability. If only 30% of fuel customers enter the store, you’re wasting 70% of your customer acquisition investment. If 70% enter the store, you’re maximizing the fuel station’s value.

Industry averages: 55-65% of fuel customers enter the store at convenience store locations. Large-format retailers (Walmart, Costco, Kroger) see 45-55% conversion because their stores are bigger and require more walking. The key is average spend per converting customer—convenience stores average $8-12 per inside sale, while Costco averages $114 and Walmart averages $37.

The profit calculation: If 60% of 2,500 weekly fuel customers enter the store, that’s 1,500 shopping trips. At $10 average spend and 35% margin, that’s $5,250 weekly incremental profit ($273,000 annually) directly attributable to the fuel station. The fuel station itself might break even, but it generates $273,000 in incremental retail profit.

Costco’s model maximizes this. Their fuel customers are already members who joined specifically to access Costco’s retail warehouse. The fuel station doesn’t need to convert cold traffic—these customers already shop at Costco. Fuel just increases visit frequency from 2-3 times monthly to weekly. Those extra visits generate incremental purchases (perishables, impulse items, new product discoveries) worth far more than fuel profit.

Track conversion rates religiously. Use license plate recognition or app-based tracking to measure what percentage of fuel customers enter the store. If conversion drops below 50%, you need layout changes, better signage, or promotional offers to drive traffic inside.

Don’t treat fuel and retail as separate businesses. If your fuel manager focuses only on fuel volume and your store manager ignores fuel customers, you’ll miss the entire point. The goal is integrated performance—fuel volume matters only if it drives retail sales.

Data Insight: How Fuel Customers Spend 40% More Inside Stores

This isn’t generic industry speculation—it’s measured data from multiple retail chains. Kroger’s 2022 investor presentation disclosed that customers who use Kroger fuel stations spend 40% more annually across all Kroger formats compared to non-fuel customers. That’s controlling for income, location, and shopping frequency.

The mechanism: fuel creates routine visits, routine visits build shopping habits, and habits drive incremental spending. Someone who visits weekly for fuel starts remembering your store for quick grocery needs. Instead of planning a separate Costco trip, they grab milk and eggs during their fuel stop. Those unplanned convenience purchases add up.

The frequency advantage compounds over time. A customer visiting monthly spends $150 per visit ($1,800 annually). A customer visiting weekly for fuel spends $65 per visit but visits 52 times yearly ($3,380 annually)—88% more annual spending despite smaller basket sizes. The weekly customer also becomes more loyal, less price-sensitive, and more likely to consolidate shopping at your location.

Casey’s General Stores built a $13+ billion business around this insight. They operate in small Midwestern towns where they’re often the only fuel option for miles. Customers come for fuel by necessity, but Casey’s captured 65% of those customers for prepared food (pizza, sandwiches, coffee). Their average customer spends $2,840 annually across fuel and merchandise, with merchandise representing 42% of spending despite being only 39% of customer visits.

The key is “since I’m here anyway” psychology. Stopping for milk at Casey’s while getting fuel takes 3 extra minutes. Making a separate trip to Walmart takes 25 minutes. That convenience value shifts small, frequent purchases to the fuel location even if prices are slightly higher.

Why Are Retailers Using Fuel to Solve Customer Retention Problems?

Customer retention collapsed in retail over the past decade. The average grocery shopper now splits purchases across 4-5 different retailers instead of consolidating at one primary store. Loyalty programs helped but couldn’t fully stop customer fragmentation—people join multiple loyalty programs and price-shop across all of them.

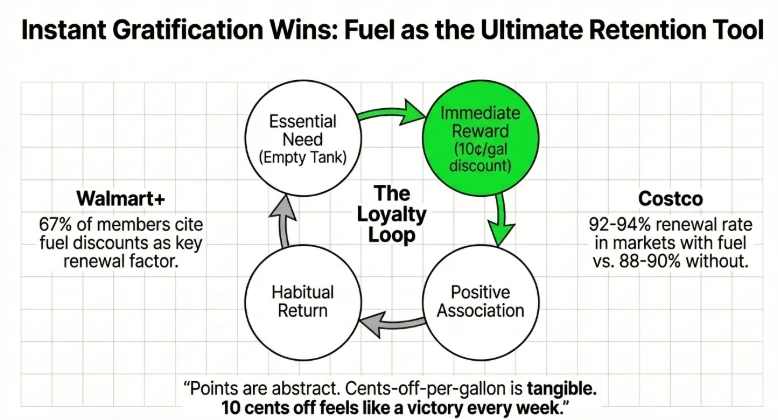

Fuel changes the retention dynamic by creating meaningful, frequent value delivery. A 10-cent per gallon fuel discount saves $52 annually for an average driver. That’s tangible value customers notice every week, unlike earning 1% back on purchases that might total $15-20 in annual rewards.

The retention mechanism: weekly fuel savings train customers to prefer your location. After 8-10 weeks of consistent fuel savings, customers develop automatic route patterns. They don’t consciously decide where to fuel anymore—they just drive to your location because it’s their established habit. Once that habit forms, they’re more likely to shop at your store for convenience.

The Loyalty Program Revolution: Fuel Discounts as Retention Currency

Traditional retail loyalty programs reward past purchases with future discounts or points. Buy $100 of groceries, earn 100 points, redeem 1,000 points for $10 off. This delayed gratification doesn’t create strong psychological bonds—customers forget about points, don’t understand redemption values, and often never redeem rewards.

Fuel loyalty flips this model. Instead of earning rewards from purchases, customers get immediate discounts on essential purchases (fuel) by linking their loyalty account. Kroger Fuel Points work this way—spend $100 on groceries, get 10 cents off per gallon immediately (up to 35 gallons). That $3.50 discount hits during the same shopping trip or within days, creating instant gratification.

The psychological impact: immediate rewards create stronger behavioral conditioning than delayed rewards. When I fill my tank and see “$0.10/gal discount applied,” my brain connects Kroger shopping directly to fuel savings. That connection reinforces every single week, building loyalty through repetition.

Walmart+ uses fuel as a membership retention tool. The $98 annual fee includes delivery, streaming, and 10-cent fuel discounts. Many members join primarily for delivery but discover they value fuel discounts more. In a 2024 member survey, 67% of Walmart+ subscribers cited fuel discounts as a key factor in renewal decisions, even though only 58% actually use Walmart fuel stations regularly. The perceived value exceeds the actual usage.

What works: Simple, immediate fuel rewards tied to loyalty program usage. Kroger’s 10-cent per gallon for every $100 spent is easy to understand and delivers value quickly. Customers don’t need to calculate points or wait months to redeem—they spend $100, they get immediate fuel savings.

What fails: Complex point systems, delayed redemption, or fuel rewards that expire quickly. Safeway tried a complicated fuel rewards system where different product categories earned different point values, points expired in 30 days, and redemption required minimum thresholds. Customer confusion killed the program’s effectiveness, and Safeway simplified it in 2019 after seeing poor engagement.

How Walmart+ and Costco Memberships Leverage Fuel for Stickiness

Paid membership programs need high perceived value to justify annual fees and prevent churn. Walmart+ costs $98 annually—customers need to believe they’re getting $98+ in value or they won’t renew. Fuel discounts provide visible, quantifiable value that members can easily track.

The math: 10 cents per gallon on 520 annual gallons equals $52 in fuel savings—53% of the Walmart+ fee covered by fuel alone. Add free delivery value (estimate $60+ for regular users), and the membership clearly exceeds its cost. This prevents the mental negotiation that kills membership renewals: “Am I really getting value from this?”

Costco uses fuel even more aggressively. Costco fuel is members-only, creating exclusive access to consistently low prices. This exclusivity makes membership feel valuable even if members don’t use fuel constantly. In markets where Costco operates fuel stations, membership renewal rates run 92-94% compared to 88-90% in non-fuel markets. Fuel alone drove 4-6 percentage point improvement in retention.

The stickiness mechanism: fuel creates weekly member touchpoints with the brand. Walmart+ members who use fuel visit Walmart locations 3.2 times weekly on average, compared to 1.8 times weekly for Walmart+ members who don’t use fuel. Those extra visits generate incremental purchases and strengthen brand preference.

What Costco does right: Consistent fuel quality, premium pump equipment (fast fill rates, clear displays), and clean facilities. Costco’s fuel stations feel premium despite low prices, reinforcing the membership value proposition. They also staff fuel stations during peak hours to help members and maintain quality, unlike many competitors who run unstaffed operations.

Don’t restrict fuel access to only high-tier memberships or charge extra for fuel benefits. Sam’s Club initially offered fuel discounts only to Plus members ($100 tier instead of $50 tier), which created frustration among basic members who felt excluded. They reversed this in 2021, making fuel benefits available to all members, which improved retention and member satisfaction.

The Weekly Visit Cycle Creating Habitual Shopping Behavior

Habit formation requires frequency and consistency. Behavioral psychology research shows habits typically form after 18-254 repetitions, with an average of 66 days for automatic behaviors. Weekly fuel purchases provide 52 annual repetitions, creating strong location habits within 8-12 weeks.

The habit cycle: cue (need fuel), routine (drive to Walmart for fuel), reward (save money + convenient shopping). After 8-10 repetitions, the routine becomes automatic. Customers don’t evaluate alternatives anymore—they just drive to Walmart because that’s their established pattern.

This habit transfers to retail shopping. Once customers habitually visit for fuel, they start thinking of that location for other needs. Need milk on Tuesday? Walmart is already their regular stop, so it becomes the default choice even for non-fuel trips. The fuel habit creates a broader location habit that captures incremental shopping occasions.

QuikTrip (Midwest/South convenience chain) built a $11+ billion business around this habit formation. They located fuel stations on high-traffic commuter routes, creating twice-daily exposure (morning commute, evening commute). Commuters develop routines: coffee and fuel every Monday/Thursday, snacks on Friday. That routine drives 65% of QuikTrip’s fuel customers to make in-store purchases at least twice weekly.

The key is making the experience predictable and reliable. Customers need consistent fuel prices (no wild day-to-day swings), consistent product quality, and reliable availability. If your fuel station runs out of premium fuel regularly or your in-store coffee quality varies daily, you’ll break the habit loop and lose the retention benefit.

What Data Opportunities Do Retailers Unlock by Entering Fuel Business?

Every fuel transaction creates data: purchase time, fuel volume, payment method, location, frequency. When tied to loyalty programs or payment apps, this data reveals customer movement patterns, purchase routines, and spending capacity.

Retailers combine fuel data with retail purchase data to build comprehensive customer profiles. Someone who fuels weekly, spends $50 per fill-up, and makes evening purchases is probably a commuter with regular employment and disposable income. Someone who fuels bi-weekly, spends $30 per fill-up, and makes weekend purchases might have different shopping patterns and needs.

This data enables targeting that wasn’t possible before. If fuel data shows someone visits every Thursday at 5:30 PM, you can send targeted offers Wednesday evening for products they might grab during their Thursday fuel stop. This timing precision increases promotion effectiveness dramatically.

Tracking Customer Behavior Across Fuel and In-Store Purchases

When customers link loyalty accounts or pay with apps, retailers can track the entire customer journey: fuel purchase timestamp, in-store entry, products purchased, basket size, payment method. This creates a complete picture of how fuel drives retail behavior.

Kroger uses this tracking to measure fuel effectiveness. They know that customers who fuel at Kroger spend 40% more annually, but they also know which specific product categories benefit most from fuel traffic. Prepared foods, beverages, and snacks see the highest lift from fuel customers—these are convenience categories people grab during quick visits.

The tracking reveals optimization opportunities. If data shows 60% of fuel customers enter the store but only 35% actually purchase anything, there’s a conversion problem inside the store. Maybe the high-margin items are placed poorly, or the checkout line is too long, or the store doesn’t carry convenient grab-and-go options.

What works: App-based tracking where customers scan a QR code or link their license plate to their loyalty account. This creates seamless tracking without requiring separate fuel cards or check-ins. Walmart’s fuel program uses the Walmart app—customers link their Walmart+ membership once, and the system automatically applies discounts and tracks behavior.

Don’t require customers to use proprietary fuel cards or complex sign-up processes. Shell tried a standalone Shell Rewards program separate from their retail partners, requiring customers to carry separate cards and track separate accounts. Customer adoption was terrible because people won’t carry 5 different fuel loyalty cards.

Personalization Strategies Based on Fuel Buying Patterns

Fuel data reveals lifestyle patterns. Someone who fuels every Saturday morning and makes large in-store purchases is doing weekly stock-up shopping. Someone who fuels Tuesday/Friday evenings and makes small purchases is grabbing convenience items between work and home.

These patterns enable personalized marketing. The Saturday shopper gets promotions for bulk items, meal planning, and family-size products. The Tuesday/Friday shopper gets promotions for prepared foods, beverages, and quick meal solutions. Same loyalty program, different messaging based on observed behavior.

Target (which doesn’t operate fuel but uses similar behavioral analysis) famously predicted pregnancy based on purchase patterns. Fuel data enables similar predictive modeling. Changes in fuel patterns (suddenly fueling more frequently, fueling at different locations, changing purchase times) might indicate life changes like new jobs, moves, or family changes.

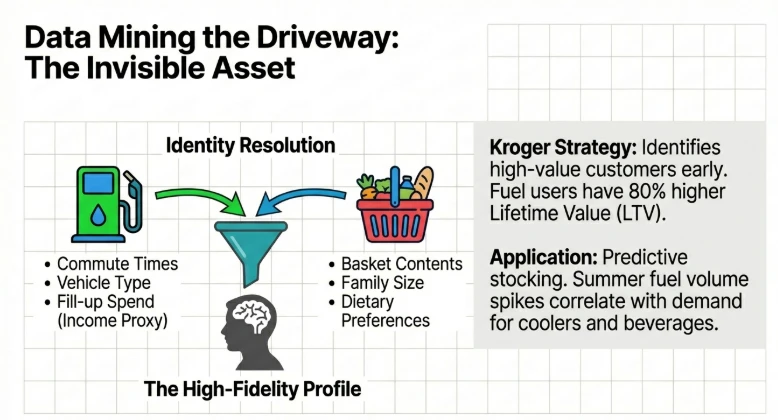

Kroger uses fuel patterns to identify high-value customers early. New loyalty members who immediately start using fuel become candidates for special retention offers because data shows fuel users have 80% higher lifetime value than non-fuel users. Kroger might send personalized offers to these customers after their second fuel visit, locking in the relationship before competitors can intervene.

The ethical boundary: use data to provide better service and relevant offers, not creepy surveillance. Customers accept recommendations based on observed behavior (“You buy milk weekly, here’s a discount”) but reject invasive predictions about personal situations. The difference is transparency—customers know you see their fuel purchases; they don’t expect you to infer their pregnancy status from them.

Predictive Analytics for Inventory and Promotion Optimization

Fuel traffic patterns predict store traffic, which enables better inventory management. If Tuesday fuel volume is consistently high, you know Tuesday in-store traffic will spike—schedule more staff, stock more grab-and-go items, and prepare for higher beverage sales.

Seasonal fuel patterns predict retail demand. Summer fuel volume increases 8-12% as people take road trips, which correlates with increased demand for coolers, ice, beverages, and snacks. Retailers can pre-position inventory based on fuel volume trends, reducing stockouts and maximizing sales during peak periods.

Weather impacts both fuel and retail behavior. Snow forecasts cause fuel volume spikes (people filling up before storms) followed by multi-day declines (people staying home). Retailers can use fuel data as an early indicator—when fuel volume spikes before a storm, it signals demand for storm supplies (bread, milk, batteries). Stock accordingly.

Casey’s General Stores uses fuel data to optimize their prepared food production. Their stores make pizza fresh daily, and production quantities were traditionally based on day-of-week averages. By incorporating fuel volume data (which shows traffic 2-3 hours before peak in-store periods), Casey’s improved forecast accuracy by 23%, reducing waste and stockouts simultaneously.

What works: Real-time dashboards that show fuel volume trends alongside retail metrics. When fuel volume runs 15% above normal, managers get alerts to prepare for higher in-store traffic. This creates operational agility that improves customer service and reduces lost sales.

Who Are the Major Retailers Entering Fuel Business and Why Now?

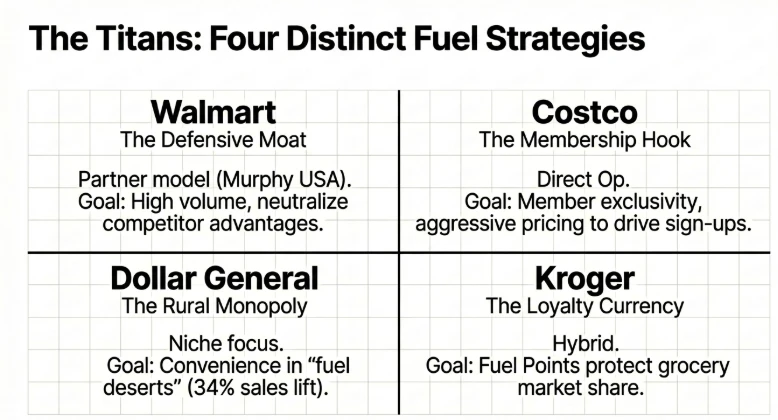

Walmart leads with 415+ locations and aggressive expansion plans. They added 45 stations in 2025 and plan another 50+ in 2026, focusing on markets where grocery competition is intense (Florida, Texas, California). Walmart uses fuel as a competitive weapon against Kroger, Publix, and regional chains that already have fuel programs.

Costco operates 700+ fuel stations globally, with roughly 600 in the U.S. Their fuel division generates approximately $25-28 billion annually, representing about 12% of total company revenue. Every new Costco warehouse includes fuel unless local zoning prohibits it—it’s standard infrastructure, not an optional add-on.

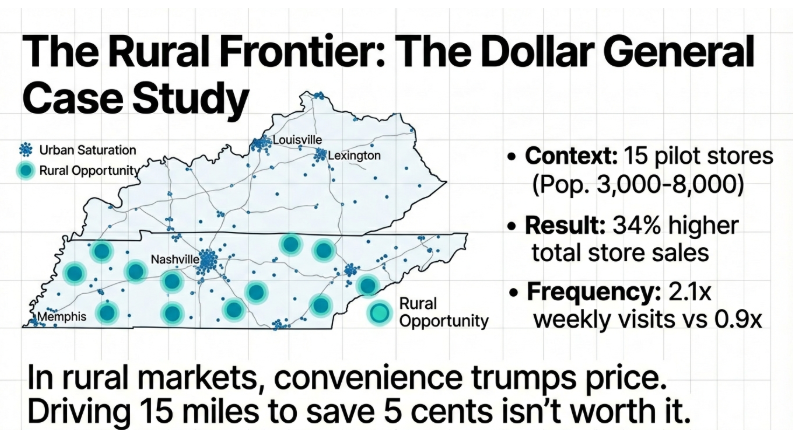

Dollar General started testing fuel in 2024 with 15 pilot locations in Tennessee and Kentucky. These small-format stations target rural areas where Dollar General dominates but lacks traffic drivers. Early results showed 34% higher total store sales at fuel locations, prompting plans for 50 additional stations in 2026.

Kroger operates 2,800+ fuel centers, the largest fuel operation among traditional grocers. They’ve operated fuel since the early 2000s but accelerated expansion in 2024-2025, adding 120+ locations. Kroger uses fuel as a defensive tool—protecting existing customers from competitor poaching by creating switching barriers.

Walmart’s Aggressive Expansion: 45+ New Stations in 2026

Walmart’s 2026 fuel expansion targets specific markets: Southeast (Florida, Georgia, South Carolina), Texas metro areas (Houston, Dallas, San Antonio), and California where competition is fierce. These aren’t random locations—Walmart is adding fuel in markets where competitors (Kroger, Publix, H-E-B) already have fuel programs.

The competitive strategy: Walmart can’t afford to let competitors have fuel advantages. In markets where Kroger offers fuel points and Walmart doesn’t, Kroger wins price-sensitive grocery shoppers. Walmart’s fuel expansion is defensive—neutralizing competitor advantages rather than creating new ones.

The partner model: Walmart works with Murphy USA, a spin-off company that operates fuel stations in Walmart parking lots. Murphy USA handles fuel procurement, operations, maintenance, and compliance. Walmart provides real estate and customer traffic. This partnership lets Walmart expand fuel without building internal fuel expertise.

The financial structure: Murphy USA pays Walmart rent for the land lease, typically $100,000-150,000 annually per location. Walmart also benefits from increased store traffic and sales. Murphy USA profits from fuel and inside-store merchandise sales (Murphy stations include small convenience stores separate from Walmart). Both companies benefit, creating aligned incentives.

What works about Walmart’s approach: They partner with specialists instead of trying to operate fuel in-house. They focus on high-volume locations where fuel volume justifies investment. They integrate fuel discounts with Walmart+, creating cross-program value. They’re selective—not every Walmart gets fuel, only locations where the economics work.

Costco’s Member-Only Fuel Strategy Driving Membership Growth

Costco fuel is exclusively for members. Non-members can’t access Costco fuel at any price, creating exclusivity that enhances membership value. This differs from most competitors, where anyone can fuel but members get discounts.

The member-only model creates FOMO (fear of missing out). When non-members see Costco fuel consistently 10-15 cents cheaper, they feel excluded from obvious savings. That exclusion drives membership conversions. Costco estimates fuel contributes to 15-20% of new membership sign-ups in markets where they operate fuel stations.

The pricing strategy: Costco prices fuel to attract members, not maximize profit. They target high volume at minimal margins, sometimes selling below cost during market spikes. In 2022, Costco lost money on fuel during a rapid crude oil price increase but maintained member pricing to preserve value perception.

The scale advantage: Costco’s 700+ stations create negotiating power with fuel suppliers. They can lock in favorable wholesale pricing, buy futures contracts to hedge against price volatility, and optimize supply chain logistics. This scale allows them to price more aggressively than smaller competitors.

The warehouse integration: Costco fuel stations sit adjacent to warehouse entrances, maximizing conversion. Members fuel, park, and walk directly into the warehouse. Average Costco fuel customer spends $114 per warehouse visit, compared to $93 for non-fuel customers. That $21 difference across millions of annual visits creates massive incremental revenue.

What Costco does differently: They invest in premium fuel equipment (fast pumps, clear displays, well-lit canopies) that makes the experience feel valuable despite discount pricing. They staff fuel stations during peak hours instead of running fully automated operations. They maintain strict quality standards, testing fuel regularly and addressing issues immediately.

Dollar General’s Rural Market Fuel Pilot Program

Dollar General operates 19,000+ stores, primarily in rural areas and small towns with populations under 20,000. These markets typically lack modern retail competition but have limited traffic drivers. Residents visit Dollar General for convenience but do major shopping in larger towns 20-40 miles away.

The fuel pilot targets this exact problem. By adding fuel to rural Dollar General locations, they create reasons for more frequent visits and larger basket sizes. Rural customers might drive past Dollar General to reach the nearest gas station—why not stop at Dollar General for both fuel and shopping?

The test locations: 15 stores in Tennessee and Kentucky, selected for demographics (population 3,000-8,000, median income $45,000-55,000, limited competition). These stores added 4-6 pump fuel stations with small canopies, minimal space requirements, and basic operations.

The results: 34% higher total store sales at fuel locations compared to control stores in similar markets. Fuel customers visit 2.1 times weekly vs. 0.9 times for non-fuel stores. Average transaction value increased from $12.30 to $16.80—customers buying more items per visit.

The expansion plan: Dollar General announced 50 additional fuel stations in 2026, targeting similar rural markets across the South and Midwest. They’re using a partnership model with regional fuel distributors who handle operations while Dollar General provides real estate and customer base.

What makes this work in rural markets: Limited competition means Dollar General can capture monopoly-like market share. Rural customers value convenience highly—driving 15 miles for cheaper fuel isn’t worth the time and gas. Dollar General fuel priced at market rates still wins because it’s the most convenient option.

Don’t try this model in urban or suburban markets where customers have 5+ fuel options within 2 miles. Dollar General’s rural strategy works because of limited alternatives, not because their model is superior. In competitive markets, Dollar General would need to price aggressively and couldn’t maintain the 34% sales lift.

Kroger’s Supermarket-Fuel Hybrid Model Success

Kroger pioneered the supermarket-fuel model in the early 2000s and now operates 2,800+ fuel centers. Their model integrates fuel directly with grocery shopping through Kroger Fuel Points—spend $100 on groceries, get 10 cents off per gallon immediately.

The integration is seamless. Customers swipe the same Kroger loyalty card for both groceries and fuel. Points accumulate automatically and apply at fuel stations without additional steps. This simplicity drives 78% participation among Kroger loyalty members—far higher than typical loyalty program engagement.

The strategic advantage: Kroger uses fuel to defend grocery customers from competitor poaching. When Walmart or Aldi opens nearby, Kroger’s fuel program creates switching costs. Customers who’ve accumulated fuel points won’t immediately switch grocers, giving Kroger time to respond with price matching or service improvements.

The financial model: Kroger fuel centers break even or generate small profits on fuel itself. The real value comes from protecting grocery sales. Kroger estimates customers who use fuel spend 40% more annually across all Kroger formats (supermarkets, convenience, specialty) compared to non-fuel customers.

The operational efficiency: Kroger places fuel centers in supermarket parking lots, sharing overhead costs. The same property taxes, insurance, and management cover both facilities. Fuel stations require minimal dedicated labor—typically 0-2 employees during peak hours, none during off-peak.

What Kroger does right: Full integration with grocery operations. Fuel points work across all Kroger formats (Fred Meyer, Ralphs, King Soopers, etc.), creating consistent value regardless of location. They place fuel stations near supermarket entrances, maximizing convenience and visibility. They partner with Shell for fuel supply, ensuring consistent quality and leveraging Shell’s infrastructure.

How Are Traditional Gas Stations Responding to Retailer Competition?

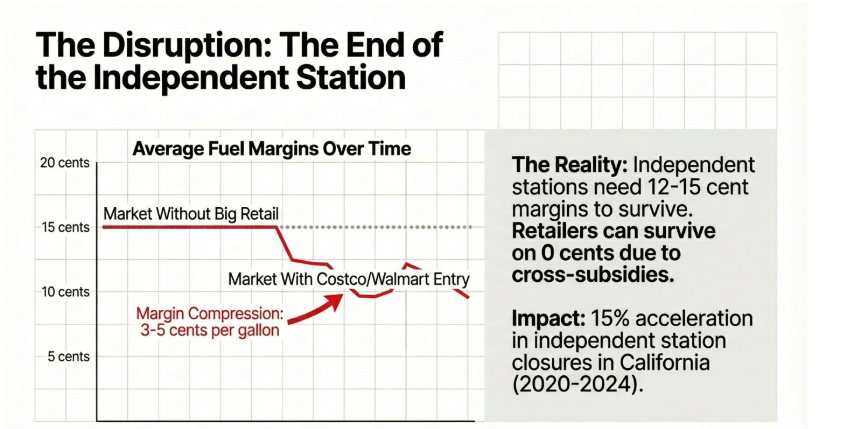

Independent gas stations are struggling. They can’t match big-box retailer pricing because they lack scale, negotiating power, and alternative revenue streams. A standalone gas station needs profitable fuel margins to survive—when retailers sell fuel at cost or below, independents can’t compete.

Major oil companies (Shell, ExxonMobil, BP) are adapting by partnering with retailers instead of competing. Shell supplies fuel to Kroger stations, BP partners with Costco in some markets, and ExxonMobil supplies various regional retailers. These partnerships let oil companies maintain fuel volume even as branded stations decline.

Convenience store chains (7-Eleven, Circle K, QuikTrip) are leaning into prepared food, beverages, and services where they have advantages. They can’t win on fuel price, so they differentiate on food quality, service speed, and location convenience. QuikTrip’s fresh-made food program generates higher margins than typical convenience store operations.

The Market Disruption Caused by Big-Box Retailers

Retailer fuel expansion reduced average fuel margins by 3-5 cents per gallon in competitive markets between 2020-2024. When Costco opens a fuel station, nearby competitors typically drop prices 4-8 cents per gallon within weeks, compressing everyone’s margins.

The volume shift: customers migrate to lowest-price options. Costco and Walmart fuel stations consistently rank among the cheapest in their markets, pulling volume from higher-priced competitors. A typical Costco fuel station pumps 4,000-6,000 gallons daily, while nearby independent stations might drop from 2,000 to 1,200 gallons daily.

The viability crisis: independent stations need roughly 1,500-2,000 gallons daily at 12-15 cent margins to cover operating costs. When margins compress to 8-10 cents and volume drops 30-40%, the math stops working. Station operators either exit the business or switch to convenience-focused models where fuel is secondary.

Regional impacts vary. In California, where Costco operates 80+ fuel stations, independent station closures accelerated 15% between 2020-2024. In rural areas where big-box retailers haven’t penetrated, independents remain viable. The disruption is concentrated in suburban markets with sufficient population to support large-format retail.

The long-term trend: fuel retailing is consolidating toward either large-scale operations (retailers, major chains) or highly specialized niche players (luxury car service stations, RV/truck-specific stations). The middle ground—typical independent stations selling fuel and basic convenience items—is disappearing in competitive markets.

Why Independent Stations Can’t Match Retailer Pricing Power

Independent stations buy fuel from distributors at wholesale prices that reflect immediate market conditions. When crude oil prices spike, their wholesale costs increase immediately. They need to pass those costs to customers plus margin, creating retail prices 8-12 cents above wholesale.

Retailers buy fuel through long-term contracts, futures hedging, and direct relationships with refiners. Costco and Walmart can smooth price volatility by locking in prices weeks or months ahead, while independents pay spot market prices daily. During volatile periods, this creates 5-10 cent pricing gaps.

The volume discount: retailers buying millions of gallons monthly get wholesale pricing 2-4 cents below what independent stations pay for thousands of gallons weekly. This structural cost advantage persists regardless of market conditions.

The cross-subsidy advantage: retailers can lose money on fuel and recover it from retail sales. Costco selling fuel at $3.29 per gallon when their cost is $3.32 is fine—they’ll make it back when that customer spends $114 inside the warehouse. Independent stations have no alternative revenue source—fuel must be profitable.

The brand disadvantage: major oil company stations (Shell, Chevron, ExxonMobil) pay franchise fees and must buy branded fuel at premium prices. These costs add 3-5 cents per gallon, making it impossible to match retailer pricing. Independent unbranded stations avoid these fees but sacrifice customer trust and quality perception.

What independents can do: Focus on service differentiators like full-service pumping (Oregon, New Jersey), specialized fuels (ethanol-free, racing fuel), or unique locations (remote highways, RV routes). Trying to compete on price against Costco or Walmart is financial suicide.

Strategic Partnerships: When Retailers and Fuel Brands Collaborate

Kroger-Shell partnerships let Kroger offer Shell-branded fuel with quality assurance while Shell maintains volume through Kroger’s retail traffic. Shell handles supply logistics and compliance, Kroger controls pricing and customer experience. Both companies benefit from the arrangement.

Costco-ExxonMobil and Costco-BP relationships work similarly. Costco operates fuel stations, major oil companies supply fuel and provide technical support. Costco gets reliable supply and quality assurance, oil companies maintain market presence and volume despite losing direct retail control.

The incentive alignment: oil companies care about volume and maintaining refining capacity utilization. They don’t necessarily need retail margins if they can move volume profitably at the wholesale level. Retailers care about customer traffic and don’t need fuel margins if they capture retail sales.

The operational division: partnerships typically split responsibilities clearly. Oil companies handle fuel procurement, quality testing, tank monitoring, and regulatory compliance (areas requiring specialized expertise). Retailers handle site selection, construction, customer service, and marketing (areas where they have existing capabilities).

What makes partnerships succeed: clear agreements about pricing control, quality standards, and cost sharing. Kroger-Shell works because both parties understand Kroger controls retail pricing (to maintain grocery customer satisfaction) while Shell ensures quality and supply reliability. Neither party tries to optimize their piece at the expense of the overall relationship.

What breaks partnerships: conflicts over pricing strategy. If a retailer wants to price fuel below cost to drive traffic but the oil company partner absorbs the loss, the relationship fails. Successful partnerships structure costs so the retailer bears the pricing risk (via wholesale purchase agreements) while the oil company gets guaranteed volume regardless of retail pricing.

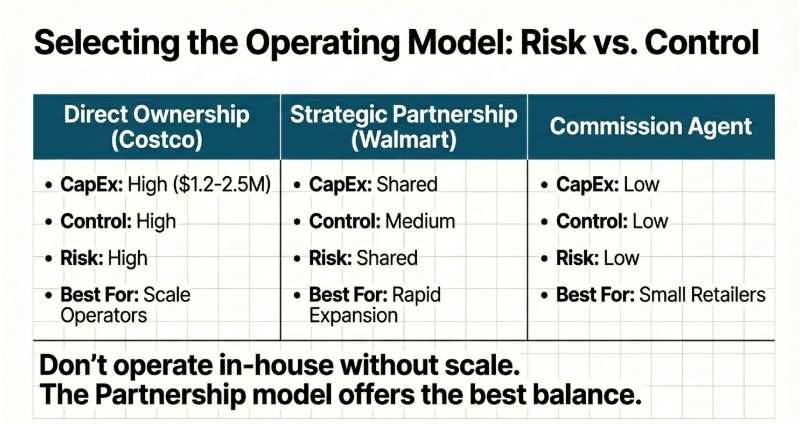

What Business Models Work Best for Retailers Entering Fuel Business?

Three primary models dominate: direct ownership and operation, partnership operations, and commission agent agreements. Each model works for different retailer types, scales, and strategic goals.

Direct ownership: retailer owns fuel infrastructure, manages operations, handles procurement and compliance. High capital cost, full control, maximum profit potential but requires fuel expertise. Very few traditional retailers use this model—it’s too complex and risky.

Partnership model: retailer provides real estate, customer base, and brand integration. Fuel operator (Murphy USA, regional distributor, oil company) handles operations, procurement, maintenance, compliance. Medium capital cost (shared infrastructure investment), shared control, profit comes primarily from incremental retail sales. Most common model for large-format retailers.

Commission agent: third-party operator leases land from retailer, operates independently, pays rent/commission. Minimal retailer capital, minimal control, lowest direct profit but still generates traffic. Used by some grocery chains and smaller retailers who want fuel benefits without operational complexity.

The Hypermarket Forecourt Model (Walmart Approach)

Walmart’s model: Murphy USA leases land in Walmart parking lots, builds and operates fuel stations, pays Walmart rent (approximately $100,000-150,000 annually per location). Walmart doesn’t invest capital in fuel infrastructure—Murphy USA funds construction and owns equipment.

The arrangement benefits both parties. Walmart gets fuel stations without capital investment or operational responsibility. They integrate fuel discounts into Walmart+ (buying discounted fuel from Murphy USA for members), driving membership value and store traffic. Murphy USA gets prime real estate, massive customer traffic, and Walmart’s brand association.

The profit flow: Walmart makes money from land lease, incremental store sales from fuel traffic, and Walmart+ membership revenue. Murphy USA makes money from fuel sales and merchandise sales in their small convenience stores (separate from Walmart). Both companies profit without competing directly.

The operational separation: Murphy USA stations are physically separate from Walmart stores, with their own convenience stores selling snacks, beverages, and basic items. This prevents channel conflict—Murphy isn’t competing with Walmart’s in-store offerings because they serve quick-convenience needs rather than grocery shopping.

What works: Zero capital requirement for Walmart, predictable lease income, full control over customer experience integration (Walmart+ discounts), and no operational complexity. Murphy USA handles everything—permitting, construction, operations, compliance, employee management.

What to watch: lease agreements must clearly define pricing coordination, brand usage, and exclusivity. Walmart can’t allow Murphy USA to dramatically underprice fuel (creating customer expectation mismatches) or overprice fuel (reducing traffic benefits). The partnership requires aligned incentives.

Strategic Partnership Model (Reliance JIO-bp Example)

Reliance JIO-bp (India) demonstrates full partnership integration. Reliance (retail/telecom giant) and BP (global oil company) formed a 51-49 joint venture to operate fuel stations and mobility services. They combine Reliance’s retail expertise, customer base, and real estate with BP’s fuel operations expertise and supply chain.

The model in Western markets: Kroger-Shell partnerships follow similar logic. Kroger provides supermarket locations and customer base, Shell provides fuel supply and operational expertise. They share infrastructure costs, coordinate pricing strategies, and integrate loyalty programs.

The value creation: partnerships combine complementary capabilities. Retailers are good at customer experience, location selection, and retail operations. Oil companies are good at fuel procurement, supply chain management, and regulatory compliance. Partnerships let each party focus on their strengths.

The governance structure: joint steering committees, profit-sharing agreements, and clear decision rights prevent conflicts. Typically, retailers control customer-facing decisions (pricing, promotions, loyalty integration) while oil company partners control operational decisions (supply contracts, maintenance schedules, compliance protocols).

What works: shared risk, shared investment, and complementary capabilities. Neither party needs to develop expertise in the other’s domain. Retailers don’t learn fuel operations; oil companies don’t learn retail customer management. Each does what they’re good at.

What fails: partnerships without clear governance, conflicting incentives, or mismatched strategic goals. If a retailer wants aggressive pricing to drive traffic while the oil company partner wants profitable margins, the partnership creates constant tension. Success requires aligned goals from the start.

Commission Agent vs. Company-Owned Operations

Commission agent model: third-party operator pays rent/commission to the retailer, operates fuel station independently. Retailer has minimal involvement and minimal profit but gets traffic benefits. Common in grocery chains that want fuel presence without operational complexity.

Company-owned model: retailer directly operates fuel, employing staff, managing supply, handling compliance. Maximum control and profit potential but requires significant expertise and management attention. Very rare among traditional retailers—usually only vertically integrated companies (oil companies with retail stations) use this model.

The commission agent advantage: zero operational complexity for retailers. The agent handles everything—employees, fuel procurement, pricing, maintenance, compliance. The retailer just collects rent (typically $50,000-120,000 annually) and benefits from customer traffic.

The commission agent disadvantage: minimal control over customer experience, pricing, or loyalty integration. If the agent prices fuel poorly or runs a low-quality operation, it reflects on the retailer’s brand. Retailers can’t fully integrate commission agent stations into loyalty programs without agent cooperation.

The company-owned advantage: complete control over pricing, customer experience, loyalty integration, and operations. Retailers can use fuel strategically (pricing at-cost to drive traffic) without negotiating with partners.

The company-owned risk: fuel operations are complex, regulated, and require specialized knowledge. Retailers who tried to operate fuel in-house without expertise faced environmental violations, supply problems, and operational inefficiencies. The cost savings from avoiding partnerships rarely justify the operational risk.

What most retailers choose: partnership or commission agent models. Only very large, sophisticated retailers consider company-owned operations, and even then, partnerships usually make more sense. The complexity-to-benefit ratio doesn’t favor direct operation for traditional retailers.

How to Choose the Right Model for Your Retail Scale

Small retailers (under 50 locations): Commission agent model. You lack scale to negotiate favorable partnership terms or expertise to operate directly. Let a third-party agent handle everything while you benefit from traffic.

Mid-size retailers (50-500 locations): Strategic partnerships with regional fuel distributors or oil companies. You have enough scale to negotiate reasonable terms but not enough to build internal fuel expertise. Partnerships spread risk and investment while giving you some control over customer experience.

Large retailers (500+ locations): Partnership model with major oil companies or specialized fuel operators (Murphy USA model). Your scale justifies customized partnership agreements, shared infrastructure investment, and deep integration with loyalty programs.

Giant retailers (1,000+ locations): Consider strategic joint ventures with full governance structures, shared investment, and long-term commitments. Reliance JIO-bp style partnerships make sense at this scale because both parties invest significantly.

The capital consideration: direct ownership requires $1.2-2.5 million per location in upfront capital. Partnerships reduce this to $200,000-800,000 (shared infrastructure). Commission agents require minimal capital ($50,000-100,000 for site prep and integration). Match your model to your capital availability.

The expertise consideration: if you have zero fuel industry experience, start with commission agents or partnerships. Don’t try to operate fuel directly—the regulatory and operational complexity will create expensive problems. Build knowledge through partnerships before considering more direct involvement.

What Operational Challenges Must Retailers Solve When Adding Fuel?

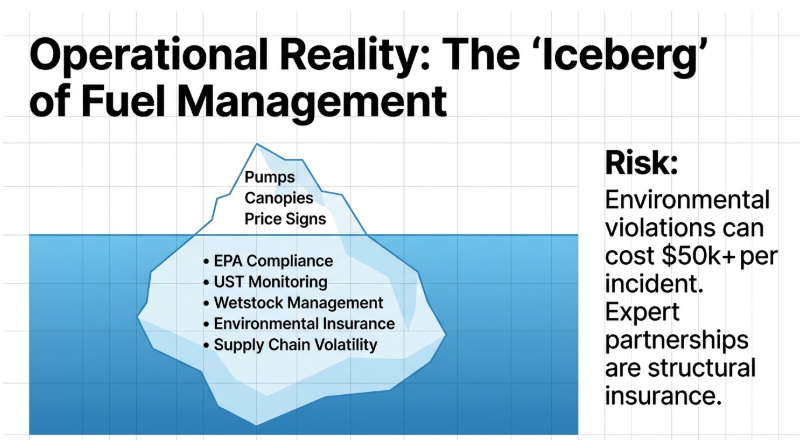

Regulatory compliance is the biggest operational challenge. Fuel operations involve environmental permits, tank monitoring, leak detection, spill prevention, and fire safety. EPA regulations, state environmental laws, and local fire codes all apply. Non-compliance creates massive liability—fines, cleanup costs, and legal exposure.

Supply chain integration challenges: fuel procurement requires relationships with distributors, negotiating contracts, managing inventory, and coordinating delivery schedules. Retail supply chains don’t prepare you for fuel supply chains—they operate completely differently.

Technology infrastructure gaps: fuel pumps need POS integration, payment processing, loyalty program connectivity, and regulatory compliance tracking. Most retail POS systems don’t handle fuel. You need specialized systems or major upgrades.

Staffing and training requirements: fuel operations require certified employees for certain tasks, safety training for all staff, and emergency response protocols. Retail employee training doesn’t cover fuel safety, environmental procedures, or compliance requirements.

Regulatory Compliance and Environmental Permits

Every fuel station requires underground storage tank (UST) registration with EPA and state environmental agencies. UST regulations mandate double-walled tanks, leak detection systems, monthly monitoring, and regular inspections. Installation requires permits, inspections, and certified contractors.

The permitting timeline: 6-18 months from initial application to operational approval, depending on jurisdiction. Urban areas with strict environmental regulations take longer. Some jurisdictions require environmental impact assessments, neighbor notifications, and public hearings before approving fuel stations.

The ongoing compliance: monthly tank monitoring reports, annual inspections, leak detection testing, spill prevention plans, and emergency response procedures. States require certified UST operators who complete specialized training. Violations trigger fines ($10,000-50,000 per incident) and potential business shutdowns.

Hire environmental consultants who specialize in fuel station compliance before starting construction. They’ll handle permitting, ensure proper installation, and establish monitoring systems. Trying to navigate EPA and state regulations without expert help guarantees costly mistakes.

Don’t skip environmental site assessments before construction. If the site has prior contamination (previous fuel stations, industrial use), you inherit liability. Proper assessments ($5,000-15,000) identify contamination before you buy or build, preventing $500,000+ cleanup obligations.

Supply Chain Integration with Existing Retail Operations

Fuel supply chains operate on daily or weekly delivery schedules based on tank capacity and sales volume. A typical station needs 6,000-10,000 gallon deliveries 2-3 times weekly. Coordinating these deliveries with retail operations (truck access, delivery timing, safety protocols) requires planning.

The supplier relationship: fuel retailers contract with distributors who deliver from regional terminals. Contracts specify pricing formulas (typically terminal rack price plus margin), delivery schedules, quality standards, and payment terms. These contracts differ completely from retail merchandise procurement.

The inventory management: fuel inventory changes constantly due to sales and temperature fluctuations (fuel expands/contracts with temperature). Retailers need wetstock management systems that track inventory, detect losses, and trigger reorders automatically. These systems don’t exist in traditional retail IT.

The payment terms: fuel distributors typically require payment within 7-10 days due to commodity price volatility. This differs from retail merchandise (30-60 day terms), affecting cash flow. Retailers need to account for faster payment cycles when planning capital requirements.

What works: partnerships where fuel operators handle supply chain entirely. They manage supplier relationships, coordinate deliveries, and handle inventory management. Retailers just need to ensure truck access and safety protocols during deliveries.

What creates problems: trying to integrate fuel procurement into existing retail procurement systems. They’re fundamentally different. Retail procurement optimizes for margin, selection, and seasonal planning. Fuel procurement optimizes for price timing, volume, and supply security. The skillsets and systems don’t transfer.

Technology Infrastructure: POS Integration and Payment Systems

Fuel POS systems need outdoor payment terminals, integration with pump controllers, real-time pricing updates, loyalty program connectivity, and compliance reporting. Standard retail POS systems don’t handle these requirements without major customization or replacement.

The pump controller integration: each fuel pump has an electronic controller that manages fueling, processes payments, and tracks volume. These controllers must connect to back-office systems for pricing updates, sales reporting, and inventory management. Integration requires specialized middleware.

The payment processing: outdoor fuel terminals face higher fraud risk and require EMV chip readers, contactless payment, and mobile wallet support. Processing fees for fuel run 1.5-2.5% (similar to retail), but the volume and transaction frequency create different requirements.

The loyalty integration challenge: connecting fuel purchases to retail loyalty programs requires shared customer databases, real-time points calculation, and discount application at the pump. This integration crosses systems—fuel POS talking to retail loyalty platforms, applying discounts based on grocery purchases.

What works: choosing fuel POS systems that have pre-built integrations with major retail loyalty platforms. Vendors like Verifone, Gilbarco Veeder-Root, and Wayne Fueling Systems offer integrated solutions designed for retail-fuel combinations. Don’t try to build custom integrations.

What fails: attempting to extend retail POS systems to handle fuel. The requirements are too different. Specialized fuel POS systems exist because fuel operations need specific capabilities (EPA compliance reporting, wetstock management, fuel pricing automation). Use proven systems instead of customizing retail platforms.

Staff Training and Safety Protocol Requirements

Fuel operations require safety training for all employees: fire hazards, spill response, emergency procedures, and customer assistance protocols. Some jurisdictions require certified fuel attendants with specific training credentials.

The specific training needs: spill containment (how to handle fuel spills safely), fire extinguisher use (different from retail fire safety), emergency shutdown procedures (how to stop fuel flow during emergencies), and customer assistance (helping customers with payment issues, fuel selection).

The certification requirements: many states require UST operator certification for personnel who manage tank monitoring, inventory, and compliance reporting. This involves 8-16 hours of training and passing certification exams. Retailers need at least one certified operator on-site or on-call.

The ongoing training: annual refreshers on safety procedures, updates when regulations change, and incident response drills. This exceeds typical retail training requirements where initial orientation suffices for most roles.

Partner with fuel operators who provide turnkey training programs. Murphy USA, major oil companies, and regional distributors offer training as part of partnership agreements. They have standardized programs covering all compliance and safety requirements.

Don’t assume retail managers can handle fuel operations without specialized training. The liability risk is too high. A fuel spill handled incorrectly can cost $100,000+ in cleanup, fines, and legal fees. Proper training ($2,000-5,000 per employee) is cheap insurance against catastrophic mistakes.

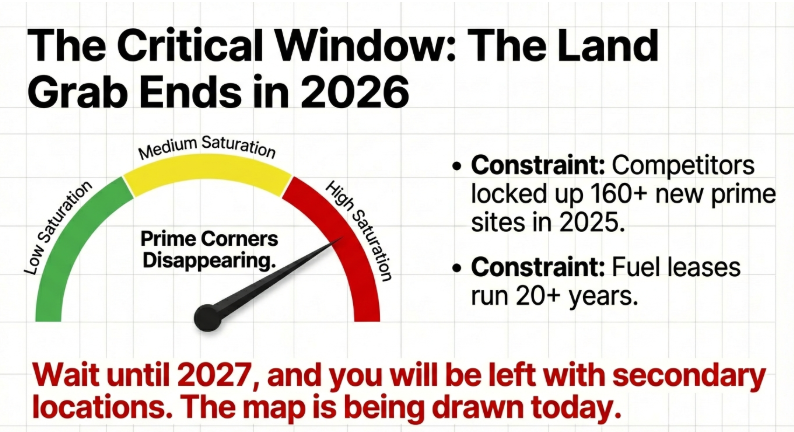

Why Is 2026 the Critical Year for Retailers to Enter Fuel Business?

Real estate availability is shrinking. Prime locations near high-traffic retail areas with sufficient space for fuel operations are limited. Once competitors secure these locations, they’re locked up for 20+ years (typical fuel station leases). Retailers who wait miss the opportunity.

The competitive dynamics shifted. Walmart, Kroger, Costco, and regional chains aggressively expanded fuel in 2023-2025. Retailers without fuel face customer retention disadvantages as competitors offer fuel rewards and one-stop convenience. The gap between fuel and non-fuel retailers is widening in customer frequency and spending.

Post-pandemic behavior changes favor one-stop shopping. Consumers consolidated trips during COVID and maintained these efficiency habits. They prefer locations offering multiple services—groceries, fuel, pharmacy, prepared food—rather than making separate stops. Retailers offering only some services lose to comprehensive competitors.

Economic uncertainty makes fuel value more important to consumers. When household budgets tighten, saving 10 cents per gallon becomes meaningful. Retailers offering fuel savings through loyalty programs gain advantage during economic stress.

Market Saturation Timing: Capturing Locations Before Competition

High-traffic locations suitable for retail-fuel combinations are finite. They need sufficient space (typically 1-2 acres for parking, fuel canopy, and tanks), highway visibility, high daily traffic counts (15,000+ vehicles), and favorable demographics (median income $50,000+).

The land grab: major retailers are racing to secure these locations before competitors. Walmart added 45 stations in 2025, Kroger added 40+, and regional chains expanded aggressively. Each location claimed by one retailer removes an option for competitors.

The long-term lock-in: fuel infrastructure creates 20-30 year commitments. Underground tanks last 20-25 years before replacement. Leases run 20+ years with renewal options. Once a competitor establishes fuel at a location, they control that advantage for decades.

The secondary locations problem: prime locations are already taken in many markets. Retailers entering late get secondary locations with lower traffic, less visibility, and worse demographics. The difference between a prime location (3,500 gallons daily) and secondary location (1,800 gallons daily) determines profitability.

Conduct market analysis identifying viable fuel locations in your operating markets. Prioritize markets where you face fuel-equipped competitors. Act quickly—every month of delay increases the chance competitors claim the best sites.

What happens if you wait: by 2027-2028, most viable locations in competitive markets will be claimed. Retailers entering after saturation either pay premium prices for less-desirable sites or skip fuel entirely, accepting permanent competitive disadvantages.

Post-Pandemic Consumer Behavior Shifts Favoring One-Stop Shopping

COVID-19 trained consumers to consolidate shopping trips. During lockdowns, people minimized outings by combining errands—groceries, fuel, pharmacy, and essentials in one trip. This efficiency habit persisted after pandemic restrictions ended.

The data: average shopping trips per household dropped from 1.6 weekly in 2019 to 1.1 weekly in 2024. Consumers didn’t stop shopping—they consolidated. Instead of separate trips to grocery stores, pharmacies, and gas stations, they choose locations offering all three.

The competitive implication: retailers offering only groceries compete for 1.1 weekly trips. Retailers offering groceries + fuel + pharmacy create reasons for 2-3 weekly visits. The frequency advantage compounds into higher annual spending.

The Amazon effect: online shopping reduced trips for non-perishables. Consumers order household goods, electronics, and clothing online, reserving in-store trips for immediacy (fuel, fresh food, urgent needs). Retailers need to dominate these immediate-need categories to maintain traffic.

What fuel solves: it’s the ultimate immediate-need category. You can’t order fuel online and wait 2 days. This forces physical visits that retailers convert into retail sales. In a world where most products are available online, fuel creates irreplaceable in-store traffic.

Economic Pressures Making Fuel Savings More Valuable to Consumers

Inflation eroded consumer purchasing power throughout 2023-2025. While headline inflation moderated, cumulative price increases reduced discretionary spending. Consumers became more price-sensitive and deal-seeking across all categories.

Fuel savings became more psychologically important. Saving $0.50 per fill-up ($1.50 weekly, $78 annually) gained attention because consumers feel fuel price changes acutely. Unlike gradual grocery inflation, fuel prices jump visibly on station signs, creating heightened awareness.

The loyalty program value perception: when consumers feel financially squeezed, tangible loyalty benefits (fuel discounts) outperform abstract benefits (points, future rewards). A 10-cent fuel discount feels more valuable than 100 rewards points worth the same $1.50 because it’s immediate and concrete.

The switching behavior: economic pressure makes consumers more willing to switch retailers for better value. Someone loyal to Albertsons might switch to Kroger if Kroger offers fuel rewards saving $80 annually. That $80 savings overcomes previous loyalty and brand preferences.

What retailers should do: market fuel savings prominently during economic uncertainty. Consumers are actively seeking ways to reduce expenses, and fuel discounts provide clear, measurable value. Use fuel as an acquisition tool when competitors are vulnerable.

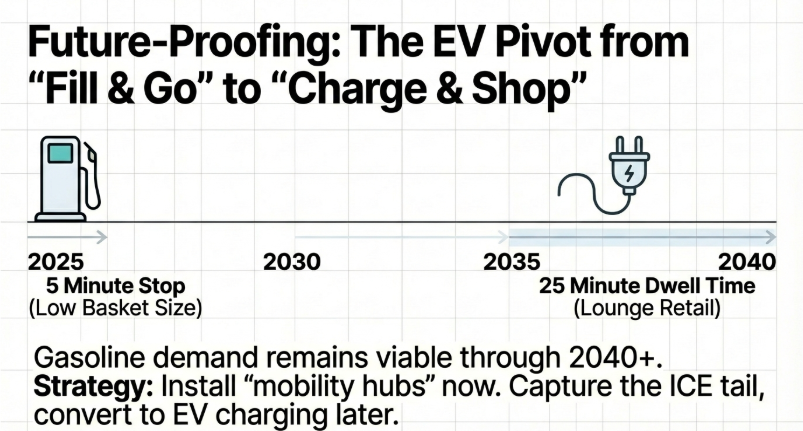

How Are Retailers Future-Proofing Fuel Investments Against EV Growth?